BROAD STREET FINANCIAL NOTES

Broad Street Notes

Analyst: Teslim K. Shitta-Bey,

Email:[email protected]

Economic Overview

It is not news that Nigeria’s economy is tanking with admission by the finance Minister that the economy has skidded into a recession with the country experiencing a second consecutive quarter of declining gross domestic product (GDP) which dipped by -0.38% in the first quarter and by another -0.56 % (by some private estimates) in the second quarter to June 2016, what does appear to be a banner headline is that despite the groaning recession the central bank of Nigeria (CBN) has chosen to jerk up interest rates to fight what it considers to be a ravaging inflation, estimated at 16.5% as at June .

Local economists have become petrified as they look on helplessly at the country’s chief financial regulator choking life out of the nation’s real sector.To be sure, a majority of companies appear to be gasping their last breadth as rising transport costs, steeper electricity tariffs and a general rise in energy expenses continues to puncture holes in their operating incomes.

Local economists have become petrified as they look on helplessly at the country’s chief financial regulator choking life out of the nation’s real sector.To be sure, a majority of companies appear to be gasping their last breadth as rising transport costs, steeper electricity tariffs and a general rise in energy expenses continues to puncture holes in their operating incomes.

Investment Highlights:

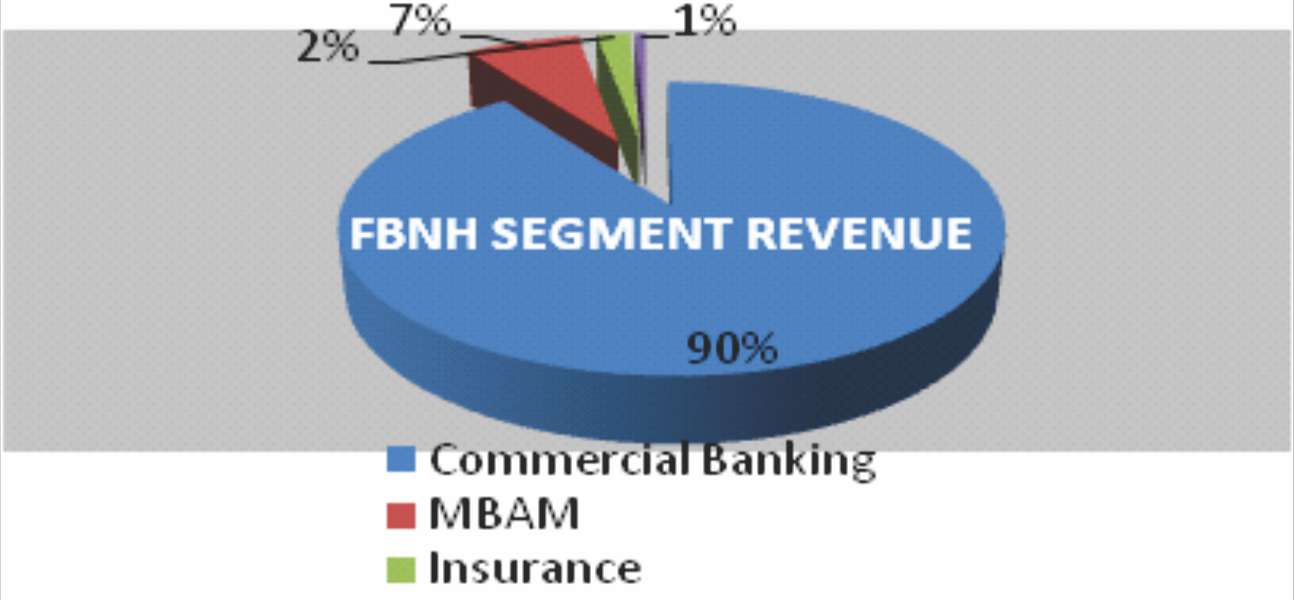

Perhaps the worst that could happen has finally taken place; FBNH’s half year result shows that the bank’s profit after tax (PAT)slid modestly by -10.5%, dropping from N40.1b in 2015 to N35.9b in 2016.The relatively weak profit posted by the bank reflects poorer loan quality and higher loan loss provisions (LLP). In the half year to June 2016, FBNH increased its loan loss provisions to 22% of its loans outstanding up from a relatively meek 4.1% in 2015. The banks year –on-year yield crashed by a thumping -53.15%, while year-to-date yield went up in flames by -34.70%. The bank’s indicated dividend yield has pinned investors to a tearful but, hopefully, temporary 4.30%.

Fundamental Highlights

The bank is bravely dealing with operating expenses as its cost to income ratio happily dropped from 61% in June 2015 to 44% in June 2016, a clear message that pork was not the flavour of the season. However, the success of the banks lean meat strategy would depend heavily on its ability to grow both its deposits and revenue.

Fundamental Highlights (Cont’d)

FBNH’S one year-forward earnings per share (EPS) estimate of N0.70 is humbling. It implies a forward price of N5.18 based on a price earnings multiple of 7.4 times. For cash-seeking investors caught in the web of double digit domestic inflation (forecast at 16.8% in July) the immediate prospects of FBNH as an investment haven is bright for contrarians.

FBNH’S one year-forward earnings per share (EPS) estimate of N0.70 is humbling. It implies a forward price of N5.18 based on a price earnings multiple of 7.4 times. For cash-seeking investors caught in the web of double digit domestic inflation (forecast at 16.8% in July) the immediate prospects of FBNH as an investment haven is bright for contrarians.

If the bank gets over its provisioning headaches in the second half of the year, it could produce a hidden value opportunity of about 54% for the brave (or silly, depending on which side of the divide you are on).

The exit of FBNH’s erstwhile chief executive officer, Bisi Onasanya,last year inauspiciously saw the banks financial performance crater. The seeds of the current problems appear to have been sown by the Onasanya management which had too casually allowed the bank to commit itself to oversized exposures to industry segments that were either imploding or on the verge of such trouble. FBNH has,in the last year or so,roiled in major exposure to the Oil & Gas and energy sectors; two sectors that have since been plagued by less than sterling operating performances.

The new management is trying to mend the banks fragile operating and credit nets by embarking on aggressive loan recoveries (this can only be mildly successful as with oil companies but perhaps more achievable in the power sector). The bank has hunkered down on costs as a proportion of income and has gradually succeeded in pulling it down.

FBNH has also begun to address the issue of systems optimization more seriously and is strategically aligning resources to value creation. The impacts of these developments may not be fully felt by stakeholders until the banks 2017 financial results. Nevertheless, by year end 2016, most of the kinks in the banks books are likely to have been worked off as it prepares for greater stability.

Market sensitivity/perception

The capital market is more than a bit uneasy about FBNH. The group has seen its share price tumble down a bumpy slope as its equity skidded from over N9.00 in mid-2014 to under N4.00 by the end of the second quarter of 2016.

Customers of the bank generally feel a sense of regression as service quality appears to have suffered as advertising also seems to have been cut back. The bank has palpably lost the verve that accompanied its century II restructuring initiative led aggressively by Onasanya in the early days after taking over leadership of the bank from erstwhile central bank governor and now Emir of Kano Sanusi Lamido Sanusi. The new MD, Adesola Adedutan is coming to grips with this reality.

Industry Perspective

Sample data of half year profit after tax (PAT) results for banks indicates a varied performance with First Bank being one of the more recent laggards.PAT at N35.9b was slightly below 10% per cent of the N40.1b posted in the comparable period of 2015 but was 295% higher than the N9.1b posted by Diamond Bank in the second quarter of the current year.

What seems to be additionally prickling investors is the delay in the half year results of three major banks classified by the Central Bank (CBN) as Strategically Important or SIB’s; the banks, GT Bank, Access Bank and Zenith Bank have each given notices of delays in the publishing of their unaudited half year accounts for 2016, a situation some observers have described as, ‘a witches hell cry presaging the occurrence of a bloody event’. This is yet to be seen, as fear appears to be the most brutal enemy of patience.