Business

Mom and pop legacy hobbles FCMB’s growth potential

– May merge or lose present corporate status in the new consolidation

Tuesday, April 20, marked exactly forty-two years since the establishment of the first private bank in Nigeria, First City Monument Bank (FCMB), by the doyen and pioneer of entrepreneurial banking in the country, late Otunba Micheal Olasubomi Balogun, with seed capital from City Securities Limited (CSL), an entity he singlehandedly founded in 1977.

With the new banking consolidation staring it in the face by which the bank is expected to raise its current paid up share capital from N127 billion to N500 billion, anxiety is high among shareholders that the doomsday may have arrived for the bank.

First known as First City Merchant Bank, the financial institution, which was the first to be established in Nigeria without government or foreign support, was incorporated as a private limited liability company on 20 April 1982 and granted a banking license on 11 August 1983.

From then on, the bank’s transformation was phenomenal. For instance, it changed name in 2001 from First City Merchant Bank to First City Monument Bank Limited after transforming to a universal bank to challenge the dominance of first generation banks like the United Bank for Africa (UBA), First Bank of Nigeria (FBN) and the Union Bank of Nigeria (UBN).

Owing to its meteoric rise, experts in the banking industry had projected that FCMB would, in the nearest future, become one of the biggest banks in the country, if not the biggest.

However, despite the huge potentials initially exhibited by the bank, FCMB has fallen far behind junior contemporaries such as Zenith Bank, Guarantee Trust Bank (GTB) and Access Bank, when it comes to total assets base, branch network and loans to deposits rate, among other performance indexes.

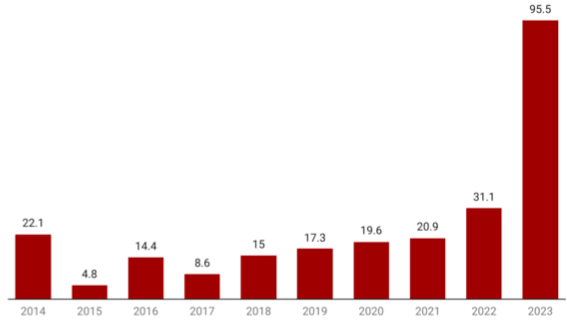

FCMB’s declared profit (N’bn) from 2014 to 2023

It would be recalled that Zenith Bank, Guarantee Trust Bank (GTB) and Access Bank were established in May 1990, February 1991 and May 1989 respectively, with the earliest among them, Access Bank, founded exactly seven years after FCMB was established.

Unfortunately, not only could FCMB compete with the top five FUGAZ banks in the areas of market capitalization and earnings, Nigeria’s first private bank even lagged behind latter days banks like Stanbic IBTC and Fidelity Bank.

This disappointing turn of fortune, findings revealed, is largely due to FCMB’s founder, Subomi Balogun’s refusal to wean the bank from his overbearing influence as a family business before his death, a decision that has ultimately come back to haunt the bank.

LEADERSHIP

Despite being a publicly quoted company, the bank has remained within the family’s control throughout the 42 years of its existence.

For instance, the late patriarch of the Balogun family, Olasubomi, superintend over the bank as chairman and chief executive officer in its first twenty years of existence, ushering in an unprecedented steady and un-interrupted growth, which earned FCMB national and international recognition as a market leader in investment banking and capital market services.

FCMB

After Subomi’s exit as CEO in 2007, Dr. Jonathan Long, who had worked under him as vice president and later president, assumed office, although effective power resided with Balogun was executive chairman. Mr. Oladipopu, Ladi, his second son, was appointed vice and Executive Director, for seven years before assuming full leadership of the bank. Ladi joined the FCMB Group Plc in 1996 as an Executive Assistant to the Chairman and Chief Executive (Late Subomi Balogun).

Under Ladi’s leadership from 2007-2017, the FCMB grew to be one of the top 10 commercial banks in Nigeria, but has not been able to break into the Top 5 league.

Unlike his father, who managed the bank for several decades as chief executive officer, Ladi was forced to step down in March 2017 as a result of a 2011 CBN policy, which limits bank MDs to a tenure of 10 years.

The Subomi family, meanwhile, found a way of keeping control of the bank in the family by installing Ladi Group CEO of FCMB Group effective March 20, 2017, allowing him to continue to call the shots.

Ladi’s successor at FCMB, Adam Nuru, formerly Executive Director, Business Development at the bank, lasted about four years in office before he was swept away by a damaging adultery scandal.

Then, stepped in the current CEO, Yemisi Edun, FCMB’s former executive director and chief financial officer, who took charge of affairs at the bank in January 2021.

While the last two CEOs of the bank, who are not Balogun by blood have so far managed the financial institution for only seven out of total 42 years it had been in existence, BH reliably gathered that the real power behind the throne was Ladi and the late Subomi Balogun.

“In fact, important decisions were not taking at the bank’s corporate headquarters at Marina, Lagos, but at Subomi Balogun’s palatial mansion on No.1, Milverton Road, Ikoyi, facing the Glover Round about while he was alive.

“Now that he (Subomi) is no more, real powers have shifted to Ladi, who overseas the affairs of the bank and FCMB Group with minimal input from his brothers, Bolaji, Jide and Gboyega”, a very close family source informed our correspondent.

While it has not been explicitly stated, Ladi Balogu has through his actions and policies communicated his determination to preserve the family legacy by holding the majority shares.

However, while the Subomi family had been able to hold firmly to their cherished bank for so long despite ceding minimal control to investors in the form of equity, the bank has been struggling to play catch-up to some of its peers established several years after without the much needed independence.

Based on BH checks, FCMB is quite far from second generation banks like Zenith Bank Plc., GTBank, Stanbic IBTC and many others. In fact, the bank had on several occasions emerged as the 10th most successful bank in the country by rating agencies using the banking industry’s performance indexes.

CAPITALISATION

Compared to other leading banks, FCMB’s N125.29 billion capitalisation figure is like a drop in the ocean. For instance, based on new computation of the paid-up capital and share premium of banks without their Shareholders’ Funds as ordered by the Central Bank of Nigeria (CBN), Ecobank leads with a minimum capital of N353.51 billion, followed by Zenith Bank N270.75 billion and Access Bank N251.81 billion.

Coming fourth is First Bank of Nigeria Holdings (FBNH) Plc with N251.34 billion, GTBank comes fifth with N138.19 billion and FCMB in distant 6th position with N125.29 billion paid-up capital and share premium. For FCMB to meet the new CBN threshold of N500billion to operate an international licence, the bank will need an additional N374.71 billion, which many financial experts believe is unattainable.

“For international banks like FCMB, the race to meet the N500billion hurdle is going to be almost insurmountable.

“It is my believe that the bank will opt to either enter into a merger agreement with other banks or downgrade, instead of searching for the elusive billions needed to meet the CBN’s target”, an economist, Tunde Awodiya stated.

CUSTOMER BASE

Based on information obtained from the bank’s website, it served over 11.7 million customers across four platforms: banking, consumer finance, investment management, and investment banking as at H1, 2023

Compared to other leading banks like GTBank, Zenith and Access, the figure is paltry. For instance, three of the banks that were established years after FCMB’s entry, GTBank, Zenith and Access Banks have 48 million, 32 million and 52 million respectively at the end of 2023.

“For FCMB to compete favourably in the industry, it must woo over more customers to its side.

“This will allow it to spread pass its high operational cost to more people. But without that, the bank will continue to struggle”, a money market analyst told our correspondent.

BRANCH NETWORK

Using FCMB’s own data, the bank has 206 branches in total. This figure is a far cry from Zenith Bank’s 393, Access Bank’s 583 and GTB’s 235. BH checks show that the bank is outside the list of top 10 banks with the most branches in Nigeria, even behind Unity Bank, a largely regional bank, which currently has 210 branches.

EARNINGS/PROFITABILITY

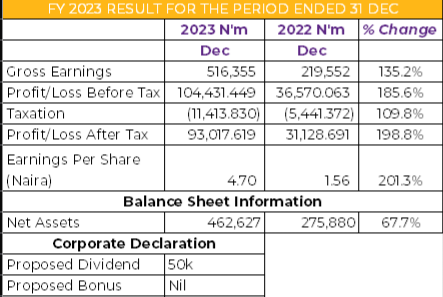

Riding on the back of its banking arm, the FCMB Group reported a 206.9% growth as it posted a net income of N95.52 billion in 2023, an improvement of N64.39billion from the N31.13 billion income recorded in 2022. The group also recorded a total comprehensive income of N145.31bn in January 2024.

A breakdown of the FY 2022 and FY 2023 reports showed that the group’s gross earnings totaled N516.79 billion in 2023, compared to N282.98 billion in 2022; interest and discount income N355.68 billion in 2023 and N219.55 billion in 2022, with interest expenses coming to N178.25 billion and N97.55 billion in 2022 and 2023.

Likewise, net interest income stands at N177.42 billion and N121.98 billion; fee and commission income N60.78 billion and N44.04 billion; fee and commission expense N16.35 billion and N10.02 billion; net fee and commission income N44.43 billion and N34.01 billion; profit before minimum tax and income tax N101.46 billion and N36.57 billion; profit for the periods N95.52 billion and N31.13 billion; foreign currency translation differences N26.52 billion and N1.59 billion and total comprehensive income N145.69 billion and N35.86 billion.

Meanwhile, Zenith, Access and GTB’s gross earnings totaled N945.6 billion in 2022 and N2.132 trillion in 2023; N167.680billion in 2022 and N729.001billion in 2023 and N539.235 billion in 2022 and N1.187 trillion in 2013 respectively.

Also, earnings per share earned by Zenith Bank shareholders in FY 2023 is N2.55; Access Bank N2.10 and GTBank N2.70. Meanwhile, FCMB’s 2023 result is still being awaited.

ASSETS BASE

According to FCMB’s own data, the bank’s total assets stood at N4.41 trillion at the end of December 2023, from N2.98 trillion in year end 2022.

On the other hand, the total assets of the three banks benchmarked against FCMB, Zenith, Access and GTBank, stand at N20.4 trillion in 2023 from N12.4 trillion in 2022; N11.7 trillion in 2023 and N15 billion at the end of 2022 and N609.3billion in 2023 and N214.2billion recorded in 2022 respectively.

Speaking on the low performance of FCMB given the pedigree of its founder, Chief Subomi Balogun, a financial analyst, who did not want his name in print, lamented that the bank has failed peoples expectations.

“The founder (Subomi) was among the earliest bankers in the industry. He could have pushed FCMB to the apex of the banking ladder, but he kept it so close because he wanted it to be a family bank, thus stifling the bank of the much needed energy to grow and compete favourably with its peers.

“Initially, he had the old legacy concept of an exclusive British or Swiss type bank for FCMB. But consolidation exercises initiated by the CBN forced him into the race to be a national bank.

FCMB

“Though quoted, FCMB is still largely a family bank. It took Subomi Balogun seven years to groom his son Ladi, who failed to really enter into his massive shoes as successor.

“I blame him (Subomi) for the current fate of the bank. He lived a good life and didn’t pay much attention to the bank, and the shareholders are the worse for it.

“And what he failed to do has caught up with the bank. To survive, its (FCMB) owners must get a good suitor for a partner or be ready to risk being swallowed up by competitors.

“The bank’s survival depends largely on how much of its Shareholders’ Funds its owners can bring back as equity.

“If they can get at least half of its encumbered Shareholders’ Fund totalling N460.74billion, the bank will be home and dry. But if not, it is likely going to be swallowed up in a merger”, the expert projected.