Business

Chinese invasion exposes Nigeria’s debt crisis

Nigerian President Muhammadu Buhari (L) and Chinese President Xi Jinping

By TESLIM SHITTA-BEY

Nigeria’s rambling debt stock continues to raise doubts amongst analysts about the African nation’s financial health. Indeed as the country’s gross domestic output (GDP) gallops at a lazy 1.5 per cent against the backdrop of huge capital expenditure sitting at about N1.7 trillion (the highest nominal expenditure in 20 years) local economists remain unimpressed. Nigeria’s incipient debt overhang has sparked debates amongst analysts and investors alike, on whether the country has been overleveraged by the current President Muhammadu Buhari administration.

To be sure, according to local economist and manufacturers, the government has made the ultimate error of concentrating borrowing exposure to sovereign and private Asian lenders, thereby creating political and economic risk factors it barely understands. According to these observers, the more debt exposure the country has to Asian countries such as China, the greater the political and economic influence Asia would have over domestic public policy. Notes economist and entrepreneur, Suraj Akinyemi, chief executive officer of Surak 713, ‘’it took the Olusegun Obasanjo administration an arm and a leg, to get the country out of its staggering $30 billion debt bind in 2005; the government had to pay off a hefty $12billion to unburden itself of an additional $18 billion in debt, the sacrifice was harsh but the benefits, in respect of lower future debt service obligation, were a whole lot better’’, but now according to Akinyemi,’’we’ve found ourselves back in the pit, with the Buhari government going into the foreign debt market like an alcoholic going to a bar, all bets are on that we will end up in the gutter’’.

To be sure, according to local economist and manufacturers, the government has made the ultimate error of concentrating borrowing exposure to sovereign and private Asian lenders, thereby creating political and economic risk factors it barely understands. According to these observers, the more debt exposure the country has to Asian countries such as China, the greater the political and economic influence Asia would have over domestic public policy. Notes economist and entrepreneur, Suraj Akinyemi, chief executive officer of Surak 713, ‘’it took the Olusegun Obasanjo administration an arm and a leg, to get the country out of its staggering $30 billion debt bind in 2005; the government had to pay off a hefty $12billion to unburden itself of an additional $18 billion in debt, the sacrifice was harsh but the benefits, in respect of lower future debt service obligation, were a whole lot better’’, but now according to Akinyemi,’’we’ve found ourselves back in the pit, with the Buhari government going into the foreign debt market like an alcoholic going to a bar, all bets are on that we will end up in the gutter’’.

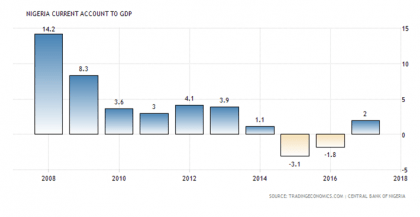

Nigeria’s debt situation, to be fair, may not be dire, but its rising size is definitely a cause for worry. When the Buhari administration came to power in 2015, the country’s total external debt stock was a comparatively modest $10.7billion in July 2015 but that figure has since risen to a staggering $22 billion or 73 per cent of the 2005 figure. By July 2017 Nigeria had already tallied up an external debt of $15 billion or 50 per cent higher than the 2015 number. By 2017 Nigeria’s Keynesian borrow to spend binge was well under way with the country’s fiscal balance tipping past a negative of 5 per cent of GDP by the end of the year. As if that was not bad enough, according to observers, the administration has gone ahead to grow fiscal spending in a frenzy of politically-motivated social transfers backed against rising international oil prices for which it has no control.

“It is kind of like a race horse gambler placing his bet on a horse that does exceptionally well when it rains but puts in an average performance otherwise; if it rains the gambler makes a tidy amount of money, but if it does not rain the gambler loses his shirt and all, now how certain are we that it will rain, or in the instance of international oil prices, how certain are we that over the next three months oil prices will stay north of $70? If oil prices drop by as much as 20 per cent, how healthy will our fiscal balance remain? In other words why are we playing a dodgy game of Russian roulette the consequences of which could prove disastrous?’’, he queries.

The nations rising debt mountain has bothered several key fiscal analysts who find it difficult to comprehend the indifferent ease with which the government has continued to pile up external loans as if, as one person put it, ‘’they are on a drunken orgy’’. The country’s debt to gross domestic product ratio has grown from a modest 7.3% in 2008 to a blinding 21.3 per cent in the first quarter of 2018, or what perhaps represents a threefold increase in the country’s external indebtedness. This has left a few development economists confused. Indeed in a recent statement, a former Senior Special Adviser to the President Millennium Development Goals and now Deputy Secretary General of the United Nations, Mrs Amina Mohammed, referred to Nigeria’s rising debt burden as a niggling sore that could fester into a malignant tumor if not checked, noting that an oil price reversal could prod another period of debt servicing challenges reminiscent of the early 2000’s when the then finance Minister and subsequent World Bank Managing Director in charge of Africa, South Asia, Europe and Central Asia, Dr Ngozi Okojo-Iweala, had to pull out all the stops in discussions with global financiers to negotiate a debt forgiveness programme that saw Nigeria pay a whopping $12billion dollar to foreign private sector creditors under a carefully curetted Paris club debt repayment/forgiveness scheme. Under the programme $18billion was written off. This, according to observers, is not likely to happen again. The recent rush to accumulate Asian debt has been seen in many economic quarters as wrong. They point to the growing debacle of other parts of East Africa where China is taking over state assets where the governments of those countries cannot pay back earlier loans or where China expresses overt interest. For example Djibouti, has become a pure Chinese ‘debt trap diplomacy’ play.

The nations rising debt mountain has bothered several key fiscal analysts who find it difficult to comprehend the indifferent ease with which the government has continued to pile up external loans as if, as one person put it, ‘’they are on a drunken orgy’’. The country’s debt to gross domestic product ratio has grown from a modest 7.3% in 2008 to a blinding 21.3 per cent in the first quarter of 2018, or what perhaps represents a threefold increase in the country’s external indebtedness. This has left a few development economists confused. Indeed in a recent statement, a former Senior Special Adviser to the President Millennium Development Goals and now Deputy Secretary General of the United Nations, Mrs Amina Mohammed, referred to Nigeria’s rising debt burden as a niggling sore that could fester into a malignant tumor if not checked, noting that an oil price reversal could prod another period of debt servicing challenges reminiscent of the early 2000’s when the then finance Minister and subsequent World Bank Managing Director in charge of Africa, South Asia, Europe and Central Asia, Dr Ngozi Okojo-Iweala, had to pull out all the stops in discussions with global financiers to negotiate a debt forgiveness programme that saw Nigeria pay a whopping $12billion dollar to foreign private sector creditors under a carefully curetted Paris club debt repayment/forgiveness scheme. Under the programme $18billion was written off. This, according to observers, is not likely to happen again. The recent rush to accumulate Asian debt has been seen in many economic quarters as wrong. They point to the growing debacle of other parts of East Africa where China is taking over state assets where the governments of those countries cannot pay back earlier loans or where China expresses overt interest. For example Djibouti, has become a pure Chinese ‘debt trap diplomacy’ play.

On the face of it, Djibouti is not an obvious choice of “strategic partner” for China or any other major global economic power for that matter. Djibouti is a tiny, poor, dry East African country with little to speak of in terms of human capital or natural resources. The country’s importance makes sense only geographically. Djibouti overlooks a strategic strait navigated by some of the world’s busiest shipping fleets while also providing a convenient docking port for naval missions to the Gulf of Aden, Djibouti is an excellent naval-base location. The country presently provides a base for France, Japan, Italy and the United States of America. With the country’s debt obligation to China, the Chinese have also decided to weigh in by opening its first permanent overseas naval base in the country in 2017.

Djibouti’s Doraleh Multipurpose Port project and its Hassan Gouled Aptidon international airport are two big-ticket transactions funded by Beijing, cumulatively worth a billion US dollars, or half of Djibouti’s gross domestic product (GDP) in 2015. The increasing lending to the country by China is clearly placing the small territories fiscal balance in jeopardy as it slurps down debt that may ultimately lead to a terrible financial tummy ache.

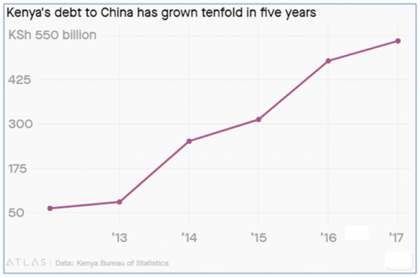

Concerns have also been raised over the threat of Kenya, one of East Africa’s largest economies, being sucked in by a similar debt dependency syndrome (China now owns over 70 per cent of Kenya’s bilateral debt). Against this background and in view of Nigeria’s upwardly drifting debt balloon, analysts have said that the government needs to rein-in fiscal spending, cut down the size of the government itself while increasing the amount of public sector savings (for example increasing the excess crude account (ECA) sum and ratcheting up the country’s sovereign wealth fund (SWF). According to Olusegun Atere, chief market analyst at one of Nigeria’s largest stock broking and investment companies, Apel Assets and Trust, ‘’the fiscal debt size needs to be carefully managed to avoid a situation where debt service continues to eat up over 60 per cent of annual budgets. Loose fiscal policy and tight monetary policy crowds out private sector investments and slows down economic growth which in turn hurts the stock market. The All Shares Index (ASI) in September has already fallen to a two year low at slightly over 32,328, a far cry from the 45,000 recorded in January.’’ Atere further notes that, ‘’if the fiscal authorities continue to issue Treasury bills to cover their serial budget gaps, interest rates will go up and national output (GDP) will come down, thereby, pushing equity investors to head for the exit. This will also put pressure on the foreign exchange rate, as foreign equity fund managers dump the Nigerian market’’.

Concerns have also been raised over the threat of Kenya, one of East Africa’s largest economies, being sucked in by a similar debt dependency syndrome (China now owns over 70 per cent of Kenya’s bilateral debt). Against this background and in view of Nigeria’s upwardly drifting debt balloon, analysts have said that the government needs to rein-in fiscal spending, cut down the size of the government itself while increasing the amount of public sector savings (for example increasing the excess crude account (ECA) sum and ratcheting up the country’s sovereign wealth fund (SWF). According to Olusegun Atere, chief market analyst at one of Nigeria’s largest stock broking and investment companies, Apel Assets and Trust, ‘’the fiscal debt size needs to be carefully managed to avoid a situation where debt service continues to eat up over 60 per cent of annual budgets. Loose fiscal policy and tight monetary policy crowds out private sector investments and slows down economic growth which in turn hurts the stock market. The All Shares Index (ASI) in September has already fallen to a two year low at slightly over 32,328, a far cry from the 45,000 recorded in January.’’ Atere further notes that, ‘’if the fiscal authorities continue to issue Treasury bills to cover their serial budget gaps, interest rates will go up and national output (GDP) will come down, thereby, pushing equity investors to head for the exit. This will also put pressure on the foreign exchange rate, as foreign equity fund managers dump the Nigerian market’’.

Indeed the administrations love affair with Sovereign bilateral Chinese credit could end badly if not reeled in. Fiscal analysts believe that the current rise in domestic debt service is unsustainable and if international oil prices tumble over the next few months, it could send the Nigerian economy careening into a deeper recession than that experienced between 2016 and 2017. Says Surak 713’s Akinyemi, ‘’ If we are going to hang ourselves by exuberant spending we should at least do it with a head that was sane and a heart that was generous to all, because as things stand today the debt pile up has had only marginal impact on growth and development’’, he insists.

Indeed the administrations love affair with Sovereign bilateral Chinese credit could end badly if not reeled in. Fiscal analysts believe that the current rise in domestic debt service is unsustainable and if international oil prices tumble over the next few months, it could send the Nigerian economy careening into a deeper recession than that experienced between 2016 and 2017. Says Surak 713’s Akinyemi, ‘’ If we are going to hang ourselves by exuberant spending we should at least do it with a head that was sane and a heart that was generous to all, because as things stand today the debt pile up has had only marginal impact on growth and development’’, he insists.