Business

$200m Paystack deal: How two Nigerians made history

BY EMEKA EJERE

United States-based financial services and software service company, Stripe has agreed to buy one of Nigeria’s biggest fintech giants, Paystack, in a deal said to be so far the biggest start-up acquisition from Nigeria.

Although the details of the deal were not immediately disclosed, TNP, a Lagos-based law firm that advised on the acquisition, said in a tweet that the deal was valued in excess of $200 million. That makes this the biggest startup acquisition to date to come out of Nigeria, as well as Stripe’s biggest acquisition to date anywhere.

It is also a notable shift in Stripe’s strategy as it continues to mature: Typically, it has only acquired smaller companies to expand its technology stack, rather than its global footprint.

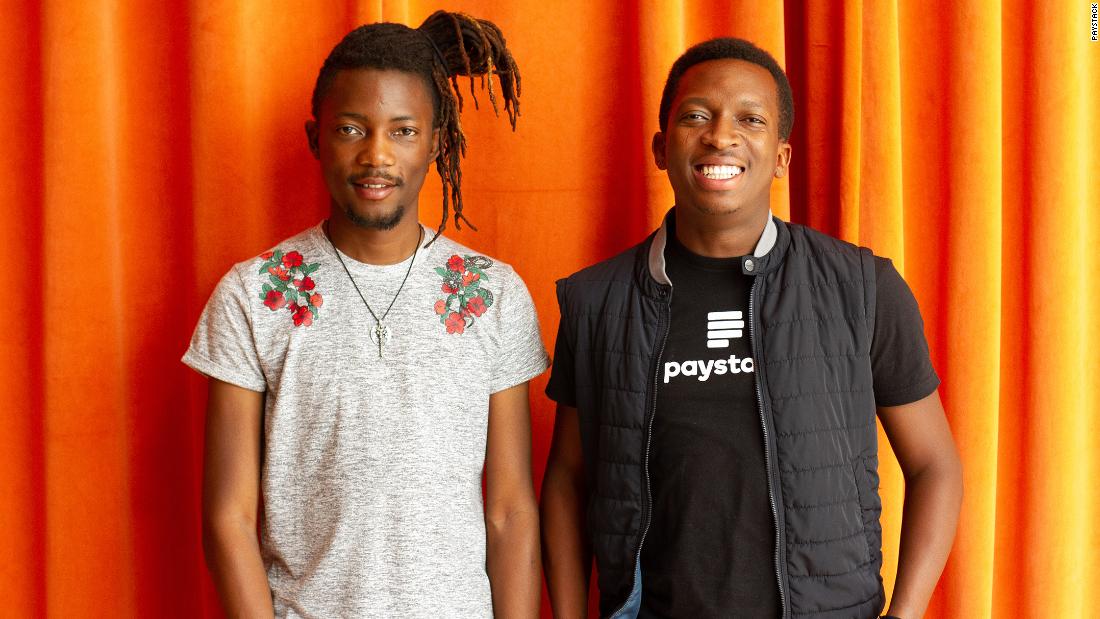

Co-founded in 2016 by Shola Akinlade, the Chief Executive Officer and Ezra Olubi, the Chief Technical Officer, Paystack is a technology company that makes it easy for organisations of all sizes to collect payments from around the world.

Paystack currently has around 60,000 customers, including small businesses, larger corporates, fintechs, educational institutions and online betting companies. Some of its business clients include telecoms giant, MTN, Domino’s Pizza and insurer, Axa Mansard.

Analysts say the deal underscores two interesting points about Stripe, now valued at $36 billion and regularly tipped as an IPO candidate. First; is how it is doubling down on geographic expansion: Even before this news, it had added 17 countries to its platform in the last 18 months, along with progressive feature expansion. And second; is how Stripe is putting a bet on the emerging markets of Africa specifically in the future of its own growth.

“There is enormous opportunity,” said Patrick Collison, Stripe’s co-founder and CEO, in an interview with TechCrunch. “In absolute numbers, Africa may be smaller right now than other regions, but online commerce will grow about 30% every year. And even with wider global declines, online shoppers are growing twice as fast. Stripe thinks on a longer time horizon than others because we are an infrastructure company. We are thinking of what the world will look like in 2040-2050.”

For Paystack, the deal will give the company a lot more fuel (that is, investment) to build out further in Nigeria and expand to other markets, CEO Shola Akinlade said in an interview.

“Paystack was not for sale when Stripe approached us,” said Akinlade, who co-founded the company with Ezra Olubi (who is the CTO). “For us, it’s about the mission. I’m driven by the mission to accelerate payments on the continent, and I am convinced that Stripe will help us get there faster. It is a very natural move.”

The fintech acquisition paves way for Stripe, which has been eyeing the African market, to “accelerate” its presence across the continent, in what observers say is a move to corner a piece of the market. To Tomi Davies, co-founder of the Lagos Angel Network and president of the African Business Angel Network, the acquisition is evidence of “inherent demand met by the ability to excel using technology-enabled innovation in spite of the odds”.

Digital payments are expanding in Nigeria and growing by nearly 500% in 2019, according to data from the Nigeria Inter-bank Settlement Scheme (NIBSS). It showed that people in Nigeria transferred N149bn ($392.1m) from their mobile devices in December 2019, up from N28.14bn in December 2018. Observers say the Paystack deal signals to Nigeria as being one of Africa’s biggest fintech destinations for VC money.

Last year, Visa paid $200m for a 20% stake in Nigeria’s Interswitch, a digital payment platform. Interswitch confirmed it reached unicorn status – a valuation of $1bn or higher – after the Visa acquisition.

Of the VC funding raised by African tech start-ups in 2019 totalling $2bn, Nigeria attracted a record high of $747m in tech investment, some 37% of all funding, according to US-based Partech, a global investment platform for tech and digital companies.

In 2016, Paystack became the first startup from Nigeria to enter Y Combinator, and the incubator is doing some follow-on investing in this round. Other strategic investors in this Series A include Visa and the Chinese online giant, Tencent.

Paystack had been on Stripe’s radar for some time prior to acquiring it. In 2018, Stripe led an $8 million funding round for Paystack, with others including Visa and Tencent participating.

In the last several years, Stripe has made a number of investments into startups building technology or businesses in areas where it has yet to move. This year, those investments have included backing an investment in universal checkout service, Fast, and backing the Philippines-based payment platform, PayMongo.

Collison said that while acquiring Paystack after investing in it was a big move for the company, people also should not read too much into it in terms of Stripe’s bigger acquisition policy.

“When we invest in startups we’re not trying to tie them up with complicated strategic investments,” Collison said. “We try to understand the broader ecosystem, and keep our eyes pointed outwards and see where we can help.”

That is to say, there are no plans to acquire other regional companies or other operations simply to expand Stripe’s footprint, with the interest in Paystack being about how well they had built the company, not just where they are located.

“A lot of companies have been, let’s say, heavily influenced by Stripe,” Collison said.. “But with Paystack, clearly they’ve put a lot of original thinking into how to do things better. There are some details of Stripe that we consider mistakes, but we can see that Paystack ‘gets it,’ it’s clear from the site and from the product sensibilities, and that has nothing to do with them being in Africa or African.”

Stripe scored a big win in financial services in the West when it developed a very quick and easy way of integrating payments into any app or website, taking what used to involve a lot of integration and negotiation and reducing it into a few lines of code.

It came just at a time when apps were starting to take off, and people were coming around to feeling more comfortable about making financial transactions online, as long as they were easy to do.