Business

Two banks lose CBN’s prime rating

OKEY ONYENWEAKU

As the Nigerian economy continues to struggle and the banks are adjusting their strategies to survive the harsh macro-economic environment, the Central Bank of Nigeria (CBN) appears to have unofficially reclassified financial institutions to differentiate the men from the boys. The performance of the banks over time is strategically important in this classification.

As the Nigerian economy continues to struggle and the banks are adjusting their strategies to survive the harsh macro-economic environment, the Central Bank of Nigeria (CBN) appears to have unofficially reclassified financial institutions to differentiate the men from the boys. The performance of the banks over time is strategically important in this classification.

The systematically important banks were eight at that time in September 2014, when the CBN issued a framework for SIBs, which was scheduled to become operational in March 2015.

First Bank of Nigeria Limited, Guaranty Trust Bank Plc (GTBank), Zenith Bank Plc, United Bank for Africa Plc (UBA), Access Bank Plc, Skye Bank Plc, Ecobank Nigeria and Diamond Bank Plc were designated as SIBs based on their impact on the Nigerian financial sector.

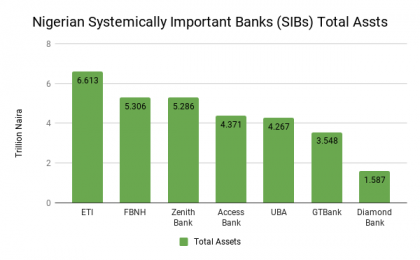

In fact, these banks have been ranked based on the following strategic indices, which include the size of their total assets, branch network, capital adequacy ratio (CAR), liquidity ratio, NPLs and so on. Most of them have continued to meet the criteria for ranking as SIBs before now.

But BusinessHallmark research has shown that with the volatility in the economy some of the banks do not appear to meet the criteria for which they were so classified. At the beginning, these lenders which were tagged ”Too Big to fail” looked strong and robust at that point in time and merited the prestigious position.

However, the trend appears to have changed. Some of these banks have skidded off the track and are no longer qualified to remain in the top ranking. One of such banks is Skye Bank Plc which appears to have failed the majority of regulatory benchmarks, forcing the CBN to axe its board and management.

Analysts also observed that Diamond Bank is undergoing a critical time and may have fallen off the cliff from the clique of SIBs while there has been serious debate where Ecobank Transnational Incorporated belongs today.

Whereas the CBN has not officially announced that any bank has been dropped from the SIB log, industry observers believe the bank which has been unable to publish its financial statements since September 2015, can no longer be considered as “too big to fail”. In 2014, Skye Bank was the fourth largest commercial lender in the country with 469 branches across the country after acquiring defunct Afribank, christen Mainstreet bank when it was nationalised by government.

While SIBs still account for over 70 per cent of total assets of the country’s banking industry, the total assets of Diamond Bank Plc shrunk in the last three years. It has dropped -61.92 per cent from N4.34 trillion at the end of 2014 to N1.65 trillion in March 2018, mainly as a result of the adverse impact of falling asset quality and the sell- off of its West African operations.

As the economic managers in Nigeria continue to fine tune strategies, there is increasing concern that the projections by both the domestic and international bodies are still elusive. That is the sad situation despite the fairly good price of crude oil at $72pbd and above.

The economy even became slower slipping from 1.9 per cent in the first quarter 2018 to 1.5 per cent in the second quarter of 2018. Therefore, there is a consensus that the financial institutions cannot grow in isolation to a strong economy. The lack of adequate direction of the economy in the last few years, analysts say appears to have a toll on the performance of the financial institutions, declined in growth year on year.

Managing Director of High Cap Securities ltd, Mr. David Adonri said the rough economic weather may have whittled down Skye Bank and Diamond Bank. In his words, ”I am reluctantly mentioning Ecobank among those that have grown weaker since that time. And I am including Fidelity Bank among the stronger ones”.

BANKS Q2 RESULTS

BANKS Q2 RESULTS

GTBANK

Guaranty Trust Bank Plc (GTBank)’s pretax profit for the half-year (H1) period ended June 30, 2018 climbed up 8.4 percent to N109.6 billion from N101.10 billion recorded a year ago.

In the same vein, profit after tax (PAT) increased 14.2 percent to N95.6 billion in H1 2018 from N83.7 billion reported the same period of 2017.

Whereas Gross earnings grew from N214.1 billion in the H1 of 2017 to N226.6 billion in the review period of 2018; indicating a growth of 5.9 percent, loan book dipped by 10.8 percent from N1.449 trillion recorded as at December 2017 to N1.293trillion in June 2018.

At the close of the business period, Customers’ deposit grew by 10.0 percent to N2.269 trillion from N2.062 trillion in December 2017.

The bank’s balance sheet remained strong with a 5.9 percent growth in total assets as the lender closed the period ended June 2018 with total assets of N3.549 trillion and shareholders’ funds of N497.1Billion.

Access Bank

Access Bank Plc, Nigeria’s tier one lender recorded a decline in pretax profit for the half-year (H1) period ended June 3o, 2018 by 11.9 percent to N45.84 billion from N52.04 billion recorded a year ago.

Post-tax profit of the lender inched up marginally 0.4 percent to N39.62 billion from N39.46 declared the same period 2017.

Gross earnings of the Bank increased from N161.90 billion in 2017 H1 period to N186.68 billion in the review period of 2018, showing an increase of 15.3 percent.

The bank proposed an interim dividend of .025 kobo per share; same amount paid last year.

FBNH

FBNH’s post-tax profit was up 22.7 per cent to N28.3N billion in first six months of 2018, the highest growth it has recorded in the last four years. The appreciation was on the back of a -15.5 per cent fall in impairment charges on loan losses to N52.7 billion and non-interest income, which grew 21.4 per cent in the first half of the year.

Analysts note that since First Bank Nigeria, the crown jewel of the Holdco’s business, resolved to restrict its single obligor limit to N30 million, and reduce the size of its risk asset, the group’s non-performing loans ratio (NPLs), which was the highest in the country’s financial industry, has continued to trend downward, dropping to 24.3 per cent in H1 2018 from 21 per cent in the same period last year. Its asset quality ratios were indicative of the progress it has made in recent times in terms of risk assets as they paint an encouraging picture with the cost of risk lowered to 4.7 per cent compared to 5.5 per cent in the first six months of 2017 and NPL coverage ratio was up to 68.2 per cent (H1 2017: 52.7 per cent). To achieve this, the group transformed its credit process by automating the evaluation and approval workflow.

The group’s decision to be conservative about its loan portfolio, having been struggling with steep toxic assets, is begging to have positive impact on its bottom-line, argued Moses Ojo, Head, Research and Business Development, PanAfrican Capital Plc.

“I expect them to post a very mild growth at the end of the year. I don’t see them achieving an elaborate performance at the end of this financial year,” he opined.

Improvement in non-interest income underpinned on 24.3 per cent uptick in e-banking, caused FBNH non-interest income to rise 21.4 per cent to N61.3 billion in H1 2018, helping to pull its gross earnings marginally up 1.6 per cent to N293.3 billion, despite Interest income dipping declined by 3.0 per cent attributable to lower yields on investment securities and constrained loan growth. The Group’s e-banking revenue has been on a steady growth since the first of 2017.

Zenith Bank

Zenith, arguably Nigeria’s largest financial lender by assets, has pleasantly surprised market pundits by announcing an interim dividend of N9.42billion or what amounts to a 30kobo per share payout.

The bank, in its half year results for the period ending June 2018 posted a profit before tax of N107.3 billion, representing a 16.5 per cent rise above the N92.1 billion achieved in the corresponding period of 2017.

While its top line fell by 15.3 per cent from N380.4billion in 2017 to N322.2 billion in 2018, the tier 1 bank’s profit after tax grew 8.2 per cent from N75.194billion to N81.737billion in 2018.

The bank’s management attributed its improved performance to keen and creative reduction in its expenses by 25 per cent.

Despite, the spike in the industry’s non-performing loans (NPL) in the first quarter through the second quarter which hovered between 8 and 10 per cent, the bank was able to keep its NPL below the regulatory bench mark of 5 per cent. This was despite the fact that the banks NPL surged ahead by 13 per cent from 4.3 per cent in 2017 to 4.9 per cent in 2018, the lenders NPL appears to be amongst the lowest in the sector.

However, Business Hallmark investigations show that whereas the bank reduced its investment in oil and gas in the last six months, the sector recorded the highest NPL of N47.019billion from the gross loans for the period. Details also show that of the gross loans of N2.109 trillion, the oil and gas received the highest proportion of about N631.973 billion, representing 30 per cent of the total loans for the period and 46 per cent NPL’s of the total(NPL 103billion).

Zenith Bank’s management team gave more attention to the Agricultural sector by increasing its credit by about 40 per cent from N63.223 billion in December 2017 to N103.185billion in June 2018. This came with a lower NPL of N854 million from the sectors NPL of N956million in December, almost balancing out the Agric sectors NPL.

Further details show that the Manufacturing sector trailed the oil and gas sector in terms of the amount of credit allotted to it by the bank with N497billion while the government and general commerce followed in that order with N337.2 billion and N228 billion respectively.

ETI

Ecobank Transnational Incorporated (ETI) reported Gross earnings of ₦384.59 billion for the period ended June 2018 compared to ₦386.82 billion reported for the period ended June 2017. This represents a 1% decrease for the comparative period in 2017.

(ETI), Profit before tax was ₦ 65.1 billion for the period ended June 2018, a 41% increase from ₦ 46.2 billion reported for the period ended June 2017.

Similarly, it’s profit after tax for the half year ended 30th June 2018 was ₦ 51.6 billion as against ₦37.7 billion recorded in H1 2017.

Ecobank Transnational Incorporated (ETI), however, reported an earnings per share of 167 kobo for the period ended June 2018, compared to 131 kobo reported for the comparative period in 2017.

Diamond Bank

Diamond Bank posted a profit before tax of 69 per cent in the second quarter ended June 2018 to N2.92billion from N9.52billion in 2017.

Gross earnings stood at N98.50 billion as against N97.89 billion achieved in the preceding period of 2017.

Managing Director of Diamond Bank, Mr. Uzoma Dozie said the bank’s non-interest income during the period grew by 6.4 per cent to N18.8 billion during the period on higher fees from retail transactions on mobile platform.

Uzoma noted that customers’ loan volume decreased by 3.6 per cent to N728.7 billion as maturities exceeded new loans during the period.

Diamond Bank Plc has strengthened its retail business segment with digital customers of three million for the second quarter ended June 30, 2018. However, analysts do not seem to be bullish on Diamond Bank which fortunes have been on the plunge for some time now.

However, there have been subtle jitters that all may not be well with the banking industry, given the depressing macro and micro-economic environment that prevailed from the beginning of 2016 to almost the second quarter of 2017.Though the economy has recorded some growth but it is still very feeble at 1.5 per cent.

Before now, declining crude oil prices, forex crisis, illiquidity, mounting non-performing loans (NPL), Treasury single account (TSA), had taken a toll on the banking institutions. However, those have eased but the challenges of slow economy, low profit margins and low capital adequacy ratio among the Deposit money banks and High NPLs still remain. Whereas these hiccups appear to be easing out, there are still concerns that the economic growth has remained feeble.

The Central Bank of Nigeria has consistently confirmed the soundness and good health of the Nigerian banks, even in 2018, there is still a debate whether three banks are still strong enough to remain as part of the SIBs.