Business

Naira takes a beating in futures market; weakens to N570/$

By FEIX OLOYEDE

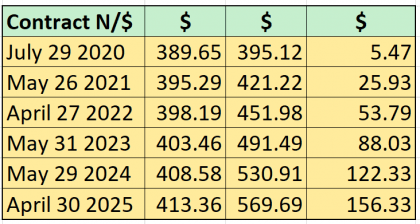

The recently repatriated Abacha loot and the approval of an International Monetary Fund (IMF) loan to Nigeria could not sway investors’ confidence in the country’s foreign exchange market as the naira weakened at the five years forwards market to N569 against the dollar on Friday. Before then, it had exchanged for N413/$.

Last week, the country received $311.80 million as part of the General Sani Abacha loot, repatriated from the United States and the Bailiwick of Jersey and the IMF disbursed a $3.4 billion loan to Nigeria to help tackle the effect the impact of the coronavirus on the country’s economy, which analysts believed should have eased the pressure on the naira.

Meanwhile, the Central Bank Nigeria (CBN) spot rate traded flat at ₦361.0/$1.00, while at the parallel market, the exchange rate strengthened by ₦5.00 to close at ₦445.00/$1.00 and the Investors’ & Exporters’ (I&E) Window, the NAFEX rate gained 5kobo to settle at ₦387.25/$1.00 on Friday.

Dr Vincent Nwani, Managing Consultant, RTC Advisory maintained that the inflow from the Abacha loot and IMF loan is good news because they are coming at a time when almost nothing is coming from Nigeria’s mainstay, which is crude oil.

“Over the past two months, Nigeria has been losing at least $35 million daily. But the Abacha loot is like a drop of water in an ocean because Nigeria is a very large economy. The IMF loan has a lot of conditionality, so it cannot be used to defend the naira,” he noted.

He believes the shortage of forex because of the fall in the prices and demand for crude oil due to impact of coronavirus on global economies, have put the country in a very tight corner that could culminate in a decision to devalue the currency.

He believes the shortage of forex because of the fall in the prices and demand for crude oil due to impact of coronavirus on global economies, have put the country in a very tight corner that could culminate in a decision to devalue the currency.

He opined, “Unfortunately, we may have allowed this decision to linger for far too long. The Abacha loot and IMF fund are not enough to stop our currency from diving to the south. The CBN does not have a choice. In life, if you do not have money, you borrow or beg for it.

“Our problem is the non-availability of foreign currencies. Even if we reform our economy now, everybody will want to see Coronavirus go away before they bring in their money. So, it is a bad time to even attract foreign investment now. “

Moses Ojo, Head, Research and Business Development, PanAfrican Capital, argued that the IMF loan and repatriated Abacha funds, were supposed to strengthen the naira, but the weakening of the local currency despite these inflows, means they were not enough to address the country’s challenge.

“Though the CBN may not immediately devalue the naira, in the long to medium term, it may be forced to further depreciate the naira,” he reasoned.

The CBN has been battling to defend the Naira as the country’s external reserves have diminished 11.68 per cent to $34.09 billion this year as global oil prices plunged below $15 last month.

Brent Crude oil has plummeted 113.11 per cent this year to $30.97 per barrel as of Friday due to a glut in the oil market as Saudi Arabia and Russia engaged in a trade war, which has however been resolved, and now leading to a 10 million barrel output cut by OPEC and its allies. The prognosis though is that the Coronavirus pandemic will yet slow down consumption significantly.

For analysts at Afrinvest, the current depreciation of the naira at the futures market simply reflects Nigeria’s exact currency risk position. “We expect stronger FX demand due to the easing of the lockdown across major economies to put pressure on the exchange rate in the near term.”

The thinking also is that pressure on the naira would further heighten when economic activities pick in the country and businesses resume import, which has been grounded since the pandemic started in the country in March.

The country’s forex crisis is further aggravated by movement of portfolio investors out of the Nigerian equity market, a trend that has continued to outweigh prospects for significantly new inflows. The Nigerian Stock Exchange’s Domestic & Foreign Portfolio Investment Report showed that while N22.49 billion came into the market as portfolio investments in March, N87.73 billion was taken out during this period.

“Also, we expect paucity of FPI inflows to persist for the rest of the year, while we also adjusted outflows for the resumption of sales to BDCs in May, albeit lower than average of January to March. With the minimal activity at the IEW in April, we believe the portion of offshore holdings of maturing fixed income ($10.6 billion between April and December) for April (estimated at $1.02 billion) is yet to be repatriated, as such we rolled it over to the rest of the year,” analysts in Coronation Merchant Bank posited.

They also projected that the country’s foreign reserves may deplete to $27.9 billion at the end of the year, despite the inflows from multilateral organizations such as the World Bank and AFDB.

They, therefore, also are hazarding that the local currency may depreciate to N410/$ at the Investors’ forex window.