Business

Tier 1 banks battle headwinds

Segun Agbaje, CEO, GTBank

By TESLIM SHITTA-BEY

Nigeria’s top tier 1 banks are still in fine shape despite growing pressure on their net interest incomes and a pummeling of local lending. Lending in the 9 months till September 2018 has declined for most of Nigeria’s money centre institutions as they cut down non-performing loans and wrestle the need for additional impairment provisions.

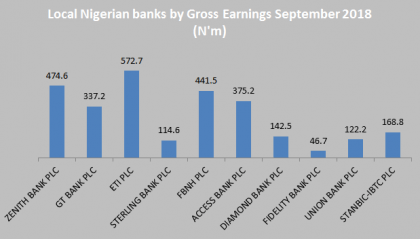

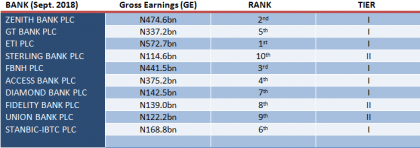

GTB cut impairments from N8.4billion in September 2017 to N1.7 billion in the contemporary period of 2018, Access Bank saw impairment provisions in the 9 months of 2018 drop from N12.8 billion in 2017 to N8.4 billion while Zenith bank’s provisions for loan impairments dipped from N47 billion in 2017 to N 14.3 billion in 2018, a downslide of 69.6 per cent. Impairments for banks have dropped just as fast or even faster than lending and gross earnings. For example gross earnings for Zenith Bank fell from N531.3 billion in the first 9 months of 2017 to N474.6 billion over the same period of 2018, representing a dip in gross earnings of 11 per cent on a year-on-year basis. This is not bad at all, as it represents about a fifth of the fall in the banks provisions for its nastier loans.

GT Bank took a different path as its gross earnings grew by 8.8 per cent from N309.9 billion in September 2017 to N337.3 billion in the same month of 2018. The bank has tactfully grown gross earnings despite the marginal drop in lending, hence ring-fencing its balance sheet against economic shocks and making the bank more appealing to shareholders and customers alike. GT’s loans and advances to customers slumped by 10.3 per cent tumbling from N1.45trillion in December 2017 to N1.3 trillion in September 2018. Analysts believe that the total year end lending figure of the bank will not differ much from that posted in December last year. Indeed, general lending by the sector

GT Bank took a different path as its gross earnings grew by 8.8 per cent from N309.9 billion in September 2017 to N337.3 billion in the same month of 2018. The bank has tactfully grown gross earnings despite the marginal drop in lending, hence ring-fencing its balance sheet against economic shocks and making the bank more appealing to shareholders and customers alike. GT’s loans and advances to customers slumped by 10.3 per cent tumbling from N1.45trillion in December 2017 to N1.3 trillion in September 2018. Analysts believe that the total year end lending figure of the bank will not differ much from that posted in December last year. Indeed, general lending by the sector  appears to have gotten stuck in a rut over the last nine or perhaps eleven months, as banks in growing numbers shy away from new credit commitments as they opt to place deposits in Treasury securities, even though the returns on these government bills have dropped from a towering 18 per cent in July 2017 to a more modest marginal rate of 10.96 per cent for three month treasuries in November 2018.

appears to have gotten stuck in a rut over the last nine or perhaps eleven months, as banks in growing numbers shy away from new credit commitments as they opt to place deposits in Treasury securities, even though the returns on these government bills have dropped from a towering 18 per cent in July 2017 to a more modest marginal rate of 10.96 per cent for three month treasuries in November 2018.

Yields on longer dated government instruments have, however, begun to rise as inflation fears and political risk considerations continue to put pressure on investor expectations. Nigeria’s ten year bond yields have risen from 13 per cent in May to 15.8 per cent in November. Bond prices have dropped as investors insist on being compensated for the country’s fragile economic and political outlook, especially with oil prices plunging to a one year low as Brent struggles to stay at $65 per barrel.

Bank balance sheets for the top tier banks may not change significantly by the year ending December 2018 as many of them have chosen to rely more on cautious routine working capital lending and aggressive reduction of their cost –to- income ratios to tide them over the slow economic growth environment (national real gross domestic product (GDP) growth has hovered between the 1.5 per cent figure for June and the 1.9 per cent International Monetary Fund (IMF) 2018 growth forecast). Rising domestic treasury yields (in other words, lower prices) will perhaps mean that tier-1 banks will feel comfortable just buying up treasuries and staying the course they have pursued from the beginning of the year. Heritage Bank director, Tony Madojemu, who once headed the bank’s board Credit Committee, notes that, ‘’ the banks have come to understand that they will have to remain reasonably liquid in the run up to Christmas and New Year activities, therefore, tying up funds in difficult risk assets at this time of the year simply won’t happen’’. Madojemu observes that banks already depressed by troublesome loan assets, ‘’are not likely to dig deeper holes to pull themselves out of the problems. Their best bet would be to repair loan books by way of recoveries, restructurings and the raising of fresh equity capital. Trying to grow loan books in times of slow growth is a fool’s game, the media hype does sounds attractive but the consequence could prove disastrous’’, he notes.

Bank balance sheets for the top tier banks may not change significantly by the year ending December 2018 as many of them have chosen to rely more on cautious routine working capital lending and aggressive reduction of their cost –to- income ratios to tide them over the slow economic growth environment (national real gross domestic product (GDP) growth has hovered between the 1.5 per cent figure for June and the 1.9 per cent International Monetary Fund (IMF) 2018 growth forecast). Rising domestic treasury yields (in other words, lower prices) will perhaps mean that tier-1 banks will feel comfortable just buying up treasuries and staying the course they have pursued from the beginning of the year. Heritage Bank director, Tony Madojemu, who once headed the bank’s board Credit Committee, notes that, ‘’ the banks have come to understand that they will have to remain reasonably liquid in the run up to Christmas and New Year activities, therefore, tying up funds in difficult risk assets at this time of the year simply won’t happen’’. Madojemu observes that banks already depressed by troublesome loan assets, ‘’are not likely to dig deeper holes to pull themselves out of the problems. Their best bet would be to repair loan books by way of recoveries, restructurings and the raising of fresh equity capital. Trying to grow loan books in times of slow growth is a fool’s game, the media hype does sounds attractive but the consequence could prove disastrous’’, he notes.

Understandably, therefore, banks have scrubbed down their lending books and kept a straight face as customers harass them over their inability to book new credit. One harried banker who declined to have his name mentioned was of the view that, ‘’we are in the business of creating risk assets that bring decent rewards at the lowest possible risk, If I can invest in treasuries at a risk free rate of return of between 12 and 14 per cent why would I want to lend to highly risky businesses at a prime lending rate of 20 per cent?’’, he argues that on a risk-adjusted basis, ‘’the risk free rate is a lot better’.

Understandably, therefore, banks have scrubbed down their lending books and kept a straight face as customers harass them over their inability to book new credit. One harried banker who declined to have his name mentioned was of the view that, ‘’we are in the business of creating risk assets that bring decent rewards at the lowest possible risk, If I can invest in treasuries at a risk free rate of return of between 12 and 14 per cent why would I want to lend to highly risky businesses at a prime lending rate of 20 per cent?’’, he argues that on a risk-adjusted basis, ‘’the risk free rate is a lot better’.

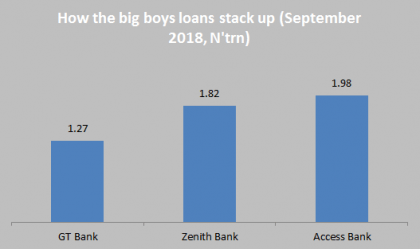

GT Bank, like its peers, has not been able to kick the lending can down the road as loans and advances to customers dropped by 7.1 per cent from N1.4 trillion over the first 9 months of 2017 to N1.3 trillion in 2018, a somewhat smaller dip compared to other top tier banks. Zenith Bank over the same period saw loans and advances drop from 2.2trillion in 2017 to 1.8 trillion in 2018, representing a 15.4 per cent dip. Zenith’s loan meltdown might be explained by the fact that it has had to cope with larger loan exposures than other banks and has had to make significantly bigger provisions for loan defaults, Its impairment charges by September was 8 times that of GT in 2018. Access Bank in turn has seen its lending slide from N1.99 trillion in December 2017 to N1.97 trillion in September 2018 broadly reflecting industry wide lending regression. Head of Research at Apel Assets and Trust, Olusegun Atere, notes that the lending shakedown, ‘’will be cold but better for the industry as banks scale down their lending portfolios and tidy up their books. In the short term this could hamper economic growth, but in the medium term cleaner loan books will lead to stronger lending growth and, hopefully, saner lending practices. Madness, including financial madness, should have limits’’, he insists.

GT Bank, like its peers, has not been able to kick the lending can down the road as loans and advances to customers dropped by 7.1 per cent from N1.4 trillion over the first 9 months of 2017 to N1.3 trillion in 2018, a somewhat smaller dip compared to other top tier banks. Zenith Bank over the same period saw loans and advances drop from 2.2trillion in 2017 to 1.8 trillion in 2018, representing a 15.4 per cent dip. Zenith’s loan meltdown might be explained by the fact that it has had to cope with larger loan exposures than other banks and has had to make significantly bigger provisions for loan defaults, Its impairment charges by September was 8 times that of GT in 2018. Access Bank in turn has seen its lending slide from N1.99 trillion in December 2017 to N1.97 trillion in September 2018 broadly reflecting industry wide lending regression. Head of Research at Apel Assets and Trust, Olusegun Atere, notes that the lending shakedown, ‘’will be cold but better for the industry as banks scale down their lending portfolios and tidy up their books. In the short term this could hamper economic growth, but in the medium term cleaner loan books will lead to stronger lending growth and, hopefully, saner lending practices. Madness, including financial madness, should have limits’’, he insists.

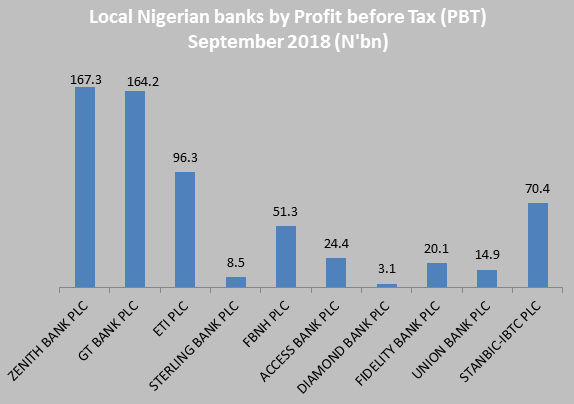

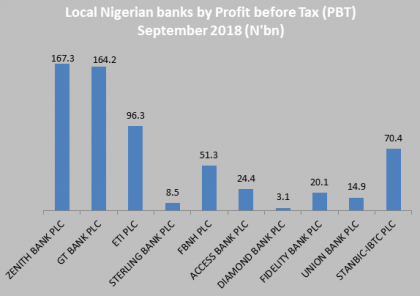

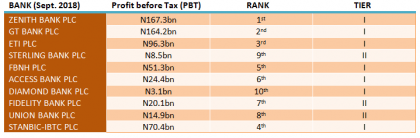

Profitability of the bigger banks has nevertheless been decent. Zenith bank held up a Profit before tax of N167.3 billion in September 2018, as against GT Banks N164.2 billion, with Access Bank strolling in at N24.4 billion behind FBNH’s N51.3 billion and ETI Bank’s N96.3 billion. Say’s Atere, ‘’profit’s in the third quarter were not earth shattering, but they equally held up nicely in the three quarters to September demonstrating that banks are coming down heavily on the poor quality of their loans and the rather fat size of their operating expenses relative to their incomes’’, he observes.

The operating environment for Nigerian banks in 2018 has been tough. Slow economic growth has meant narrower opportunities for banks to lend into rising revenue cycles as manufacturers and retailers find that consumer demand has stayed sluggish. Rising international oil prices has increased fiscal revenues which many had hoped would translate into higher public and private sector spending thereby stimulating domestic demand but that has not happened. Fiscal incomes have gone into social transfer projects that as at yet have not significantly raised living standards. Economists note that this relates to a low domestic consumption multiplier.

Low domestic productivity combined with high domestic interest rates has kept industrial output low and raised the demand for savings, thereby limiting the expansionary impact that would have occurred with lower cost of credit and higher private consumer spending. Be that as it may, Nigeria’s first tier deposit money banks are still in the business of making money, even if the sound of their teller points are quieter and their bottom lines pull up like a young ladies miniskirt.