Business

Mounting external debt burden threatens Nigeria’s growth projections

Analysis of Nigeria’s 2024 spending on foreign debt service so far suggests a disturbing trend of a public finance pressure, lending credence to unhealthy projections emanating from reputable agencies.

For instance, global credit ratings agency, Fitch, has, in its latest credit outlook for Nigeria, projected that the country’s external debt servicing would rise by $400m to $5.2bn in 2024.

This is at variance with President Bola Tinubu administration’s insistence to focus more on domestic borrowings from the capital market for its developmental projects.

The government is also giving the impression of a determination to stop the vicious cycle of overreliance on borrowing for public spending and the resulting stress on the management of scarce government resources caused by debt service.

However, Data from the international payment segment of the Central Bank of Nigeria (CBN) website revealed that debt service payments increased steadily between January and March and over the past few years. This has seen the Federal Government spend about $1.12bn on foreign debt service payments in the first quarter of 2024.

A monthly breakdown of the debt service payments revealing a fluctuating yet consistently high expenditure pattern shows that the government started 2024 with a significant debt servicing obligation of $560.52m in January. This sum alone exceeded the entire debt servicing expenditure of January 2023 ($112.35m) by nearly five times.

In February 2024, the debt servicing payments were somewhat moderated but remained substantial at $283.22m. It is lower than January’s massive outflow, and February 2023’s debt servicing of $288.54m.

March 2024 continued the trend but at a lower figure, with Nigeria expending $276.17m on debt servicing. While this represented a slight decrease compared to February and a far lesser decrease from March 2023’s $400.47bn, it was still a notable expenditure, further burdening the country’s fiscal position.

It was further observed that Nigeria spent about 70 per cent of its dollar payments to service external debts between January and March 2024.

According to data from the CBN, out of the $1.61bn in total outflows made during this period, a substantial amount of $1.12bn was directed towards servicing external debt. This figure represents a hefty slice of the nation’s financial resources and indicates a significant increase from the previous year when it was 49 percent in Q1 2023.

Debt service

The Federal Government is targeting a 3.76 percent economic growth in the 2024 fiscal year, while the International Monetary Fund (IMF) in its World Economic Outlook for April, adjusted Nigeria’s economic growth forecast upward to 3.3 percent.

Return to Eurobond

Recall that the Federal Government had in March enlisted the expertise of leading global investment banks, including Citibank NA, JPMorgan Chase & Co, and Goldman Sachs Group Inc., to guide its June Eurobond issuance. It also appointed Standard Chartered Bank and the Lagos-based financial advisory firm Chapel Hill Denham to consult on this venture.

The Eurobond issue, which would be the first since 2022, marks the country’s return to the international bond market after a two-year pause. In March 2022, the country raised $1.25 billion through Eurobond issuances.

This development, as reported by Bloomberg and informed by sources close to the transaction, underscores the intent of Africa’s leading oil-producing nation to re-engage with global financial markets in order to bolster its fiscal budget

The external funding appears crucial for Nigeria as it seeks to finance a substantial budget deficit outlined in President Bola Tinubu’s N28.8 trillion ($18 billion) spending blueprint for 2024, targeting a fiscal shortfall of N9.8 trillion, or 3.8 per cent of its GDP. The deficit is expected to be bridged through local and international borrowings and assistance from global financial institutions.

In December last year, the Minister of Finance and Coordinating Minister of the Economy, Wale Edun, hinted that Nigeria was contemplating issuing Eurobonds later in the year if the rates are considerably lower, stating that major issuers have informed the country of the possibility this year.

He noted, “It is a matter of discussion at the moment, but we think we will get the support because we are continuing with our reforms.”

Cause for concern

The World Bank, in a recent statement, expressed deep concern over the escalating debt service costs that are burdening developing countries worldwide. The World Bank’s Chief Economist, and Senior Vice President, Indermit Gill, emphasized the gravity of the situation, highlighting the potential for a widespread financial crisis if immediate and coordinated actions are not taken.

According to Gill, the combination of record-level debt and soaring interest rates has set many developing nations on a precarious path that could lead to economic distress and tough decisions regarding the allocation of resources.

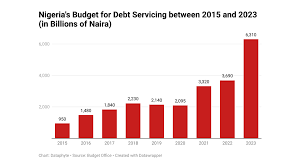

The Debt Management Office had stated that Nigeria incurred a debt service of $3.5bn for its external loans in 2023. This was a 55 per cent increase from the $2.6bn incurred in 2022 as debt service-related payments for the country’s external debts.

On the external debt, Fitch said external financing obligations through a combination of multilateral lending, syndicated loans, and potentially commercial borrowing will raise Nigeria’s debt servicing from $4.8bn in 2024 to $5.2bn in 2025. The anticipated servicing includes $2.9bn of amortisations, including a $1.1bn Eurobond repayment due in November.

Fitch’s report read: “External debt service will rise in 2025. Government external debt service is moderate, expected at $4.8bn in 2024 and $5.2bn in 2025 (with $2.9bn of amortisations, including a $1.1bn Eurobond repayment due in November). The government plans to meet its external financing obligations through a combination of multilateral lending, syndicated loans, and potentially from commercial borrowing.”

Analysts see this disclosure as underscoring the nation’s high debt service-to-revenue ratio posing significant fiscal constraints.

In 2023, the FGN’s external debt service payments increased by US$1.1bn to US$3.5bn in FY2023, comprising US$1.9bn and US$1.6bn in market and non-market debt payments, respectively. FG also projected a spending of N8.25tn to service its debt in 2024.

David Adonri, Executive Vice Chairman at Highcap Securities Limited, in a reaction said, “Against experts advice, public borrowing continues with undiminished intensity. Increasing public borrowing makes fiscal policy expansionary which is in opposite direction to the contractionary monetary policy that the CBN is running to rein in inflation.

“Without commensurate rise in public revenue, Nigeria is heading for a situation where debt service ratio may exceed 100%. Excessive public borrowing, added to tight monetary policy is already escalating the cost of credit and crowding funds away from production.

“External borrowing is a more dangerous proposition than domestic debt which can be extinguished by sovereign authority of government. Any sovereign default on external debt is visited with dire consequences.”