Business

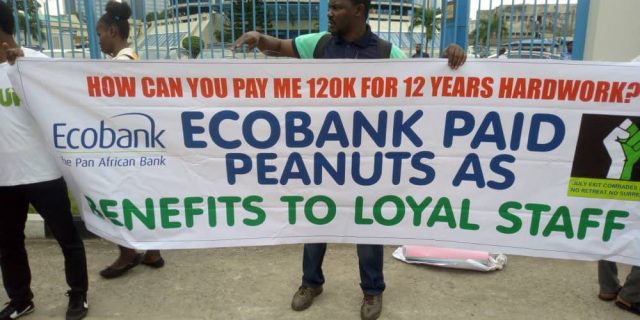

Mass sackings rock Ecobank: Disengaged staff allege victimisation and breach of contract

By JULIUS ALAGBE

Pan African bank, Ecobank seems to have been getting more than it bargained for as the downsizing that took place recently is producing some intended consequences. The bank has been making frantic efforts to stabilise its operations and improve on performance, which had suffered some bad patch in the past few years especially after its acquisition of Oceanic bank.

For some experts downsizing as a strategy for cost reduction is dead end. It has implications for cost and productivity as well as other sundry issues if not transparently and implemented with fairness. But Ecobank’s action seems to be a justification for using contract staffers which casts aspersion on the banking industry ethos.

“Bankers are rule breakers on their own – and most time don’t care about whose ox is gore”. Hasn’t Ecobank proven to be so? The bank has put 1,200 families on the streets without much consequence said a banker who preferred anonymity.

Perhaps, with intention to reduce its financial burden, 1200 contract staffers were laid off, yet the Pan-African bank claimed no wrong doing. There were issue with severance payment, which means the intention is clearly to reduce its financial burden. But once again, the action beats down corporate governance stance at Ecobank.

Ecobank expects its operating income to remain flat in 2019 as the Group seeks to achieve moderation in cost to income ratio with 62% as target. The management also expects to grow profit before tax by 8% maximum and remains focus at improving assets quality. Thus, NPL ratio target for 2019 is pegged between 8% and 10%.

“We are not under obligation to renew the contract with a third party outsourcing firm”, Ecobank said convincingly and the National Union of Banks, Insurance and Financial Institutions Employees, NUBIFIE, has also threaten a show down with the bank. The case for outsourcing in Nigeria banks is in a sorry state as consultants at LS intelligence put it.

Ecobank battle against rising cost

Whenever a bank operations hit iceberg, there is only one prevailing strategy, albeit dead one at that – downsizing. Ecobank numbers show some clues. The Group’s operating expenses ballooned in the recent time, and elevated personnel cost has been one of the key drivers. Unfortunately, fat cats were least affected in the mini-restructuring, but contracts staffers were primary target.

It has been alleged that vested interest in the bank pull the plug on the battalion of contract staffers to pave way for certain interests connected to the Managing Director to take over the outsourcing contract. For reckoning, the past few years have been so challenging for Ecobank Transnational Incorporated (ETI), Pan-African bank holding company with presence in about 36 African countries.

Analysts are of the view that Ecobank brand scorecard was hard hit due to lack of transparency in its reporting of the asset quality, poor credit origination and monitoring. In the past few years, ETI was exposed to poor corporate governance, crisis in succession and myriad of corporate contradictions that complicated its governance stance as found in the internal management of the Group with total assets that closed financial year 2018 at N8.223 trillion or $22.582 billion.

Yet, there is a monster the new team is yet to be able to tame – high cost to income. And now, the management is handling it poorly and unemotionally just as pristine capitalists. The Group cost to income ratio settled at 61.5% in 2018 as against 61.8% in 2017. Though, the cost declined but when compared with the size of the Group’s balance sheet and operational performance it is insignificant.

What this means is that the Group is burning more than 61% of its revenue to settled operational overheads. This makes the profit conversion, which is the amount of the earnings that the Group was able to convert to profit or free cash flow, low. But the new management team is upturning the past anomalies in the administration of the bank and the numbers have started coming up. In June, 2018 Moody, a rating agency, assigned B2 first time issuer rating on ETI, reflecting increased confidence at the time. Moody, an international agency, observed that the ratings reflect the group’s stable funding and liquidity profile, expansive geographic and business diversification, recovering profitability.

There have been signs of commitment to improve profitability, and boost investors’ perception of the bank and consequently improve shareholder value.

Mr. Ade Ayeyemi, the Group Chief Executive Officer said, “Our financial performance in 2018 was remarkable in many ways and reflected the meaningful and significant progress that we have made against the priorities that we set in our ‘Roadmap to Leadership’ strategy.

“These strengths are balanced against the Group’s high — but potentially moderating — asset risks and modest capital buffers, which are largely legacy issues that the bank’s new management is pro-actively addressing as part of a broader strategic plan. The new strategy also introduces digitalization and cost-cutting initiatives”.

Cardinalstone Partners noted that following the economic down-turn that exposed the weakness of the Group, ETI’s management has shown resolve to strategically reposition the Group for profitability. ETI’s deposits have historically been stable, while the bank also has access to longer-duration market funding, which helps support its liquidity management and better match the duration of its assets and liabilities.

At the end of end of financial year 2018, deposits from customers increased by $733 million, or 5%, to $15.936 billion. This, excluding the impact of FX translation, deposits increased by $2 billion.

Earnings on the rise

In 2018, the Group recorded a significant improvement in its earnings generating capacity, supported by the new management team’s focus strategy and reorganisation initiatives that have led to cost cutting and lower provisioning requirements.

Ayeyemi said; “We delivered a 51% growth in profit before tax to $436 million and generated a return on tangible equity of 21%. Our cost-of-risk of 2.4% was an improvement on 2017 and demonstrated the progress that we have made addressing credit quality issues and enhancing internal control processes”.

But with ETI reporting currency in the U.S. dollar, the high volatility of many African currencies due to the region’s economic dependence on commodities will continue to affect stability and predictability of earnings, Cardinalstone Partners stated.

Management transfers legacy loans to SPV

As part of efforts to clean the house, Cardinalstone stated that prior to the release of its financial results in 2016, ETI’s transferred cumulative impairment charges on bad loans which was aboutN282 billion, and its Nigeria loan portfolio has contributed about 76%to total impairments.

The special purpose vehicle, SPV, was expected to recover of the total legacy loan portfolio worth $780 million. The portfolio was made up of impaired credit assets inherited from Oceanic Bank as well as other delinquent assets impaired as a result of the ongoing FX crisis and poor due diligence at origination. In 2016, Cardinalstone analysts noted that, of the $780 million legacy loans, ETI provided for $517 million of which $400million was completely written off.

Between 2013 and 2017,

In financial year 2013, ETI’s cost of funds was 3.1%, and then it moved up to 3.4% at the end of financial year 2014. Meanwhile, the Group cost to income ratio was 70.1% in 2013 before it was brought down to 65.4% in 2014.

On every share ranked for dividend, ETI earned N4.12 in 2014. This means that the Group has been accessing cheap funding, derived from its ballooned deposits but the Group operations have been burning more cash as reflected in high cost to income ratio.

ETI’s shareholders’ fund increased by more than 255% between 2013 and 2014 on the back of shareholders’ confidence for strong stream of earnings. Then, return on average equity closed financial year 2014 at 20.18%. And the group total assets rested at N4.5 trillion, having expanded by more than 25% from N3.599 trillion in 2013. Of the N4.008 trillion total liabilities in 2014, total deposits accounted for N3.513 trillion.

In 2015, the parent company blew an alarm. ETI released a statement which stated that profit for the year ended 2015, is expected to be materially lower than expected. In 2015, ETI recorded cost to income ratio that settled at 63.9% before it moderated to 61.1% in 2016 the same time when cost of funds berthed at 3.2%. Total deposits moved from N3.559 trillion in 2015 to N4.773 trillion in 2016.

From N502.9 billion in shareholders, the group recorded a 7% upsurge which shifted total equity size to N538 billion in 2016.Infinancial year 2016, the Group had total assets worth N6.255 trillion, having expanded by more than 33% year on year from N4.694 trillion.

In financial year 2018,

ETI earned N5.57 on every share ranked for dividend in 2018 as against N3.81 in 2017. That represents 45.97% year on year raise. Its price to earnings ratio receded to 2.37 times from 4.71 times in 2017. The Group total assets expanded 19.81% from N6.864 trillion in 2017 to N8.223 trillion at the end of financial year 2018. The group total liabilities which jerked up by 22.01%, thereby outpaced the growth in total assets.

The Pan-African bank holdings shareholders fund went down marginally to N660.073 billion from N664.657 billion in the preceding year. Its gross earnings rested at N773.338 billion in the financial year 2018. This was 1.27% above N763.633 billion the group earned in 2017.

But, its interest earnings assets yielded lower in 2018 compare with the amount raked in at the end of financial year 2017. The numbers showed that ETI’s interest income was N475.144 billion followed a 1.21% drop against N480.94 billion in 2017.

Meanwhile, interest expenses rose 2.47% from N181.617 billion to N186.105 billion. This means that while it cost ETI N37.76 on every N100 income generated from interest earnings assets in 2017, the year 2018 saw an increase to N39.17.

At the operational level, the group was able to reduce operating expenses on the back of reduction in numbers of member of staffs on its payroll in 2018. The analysis shows that operating expenses declined by 1%, to $1.123 billion. Excluding the impact of FX translation, expenses were flat.

Meanwhile, costs associated with systems development and head office investments led to a 2% increase in depreciation and amortisation expense. Other operating expenses decreased by 2%, driven by lower expenses from rent and utilities and insurance.

Overall, the decrease in operating expenses reflected the accrued benefits from the restructuring exercises in the last two years. The cost-to-income ratio, as a result, improved to 61.5% from 61.8% in 2017, despite slower revenue growth.

Meristem Securities Limited noted that the bank’s cash management services across its wide West African coverage remains a key driver of income and the analysts expect this to continue in 2019. The firm also expect to see an increase in interest income owing to the significant loan growth of 30.12% in the fourth quarter of 2018; hence, it projected loan growth of 3.20%.

The Securities firm noted that with regards to interest income, non-interest income and gross earnings, the analysts project growth of 10.94%, 11.05% and, thus, 10.72% respectively. The results showed that lower asset yield pressures net interest margin, yield declined from 6.20% to 5.90% by 2018, mainly due to the lower yield on earnings assets across the Nigerian environment and the switch of asset blends towards investment securities as against loans.

In 2018, operating expenses grew moderately by 0.72%, while impairment charges declined considerably by 34.87%, owing to the impairment write-backs of about $318.75 million. Like its peers in the industry, Ecobank is still bearish on lending. Most big balance banks leveraged on high yield environment to shored up performance in 2018. The group recorded a decline in loan amount.

The numbers showed that net loans and advances to customers berthed at $9.167 billion, which means it receded by 2%. But, compare with the apex bank benchmark, non-performing loan ratio declined to 9.6% from 10.7% in 2017. This means that about 10% of the group gross loans is exposed to default.

In presenting its financial statement the Group moved away from using the CBN Official Rate of N306 and instead adopted NAFEX rate N364 for translating its financial statement. Analysts said that what this means is that the Group financial statement would be volatile; as adjustment at NAFEX would result to either gain or loss in financial statement translation.

The spokesperson of the bank Mr. Austin Osopka said that the management was in a meeting with the union which had besieged the office and they will have a statement on the outcome which may address all the issues