Total Plc, at its Annual General Meeting (AGM) held in Lagos, recently proposed a dividend of N9.00 per share and was duly approved by its shareholders making a total dividend pay-out of N11.00 per share in 2014, having given out an interim dividend of N2.00 per share earlier.

This largesse has overshadowed the performance of the company and the negative sentiments of investors towards the stock in the first quarter of 2015.

An above average performance in the audited 2014 result highlights the difficult terrain faced by the company and other oil majors in Nigeria in the past one year. Although the company was able to grow revenue by 1% from N238.163 billion in the preceding year to N240.618 billion, it was not able to grow profit as it declined in that arena by -17% to N4.423 billion from N5.334 billion.

It might be safe to conclude that the company performed below expectation from its results. However, a cursory look at issues surrounding the company or issues at play at that time which invariably affected its performance, reveals that the challenges and difficulties in its operating environment actually impacted heavily on its audited result. In spite of the security, regulatory, social and economic challenges, it was able to make profit and appropriated a mouth-watering dividend to its shareholders.

Analysts believe that the oil and gas sector being the major contributor to the revenue of the nation should reflect on its day to day performance on the stock exchange. Prominent among these challenges is the decline in global crude oil prices in the last one year.

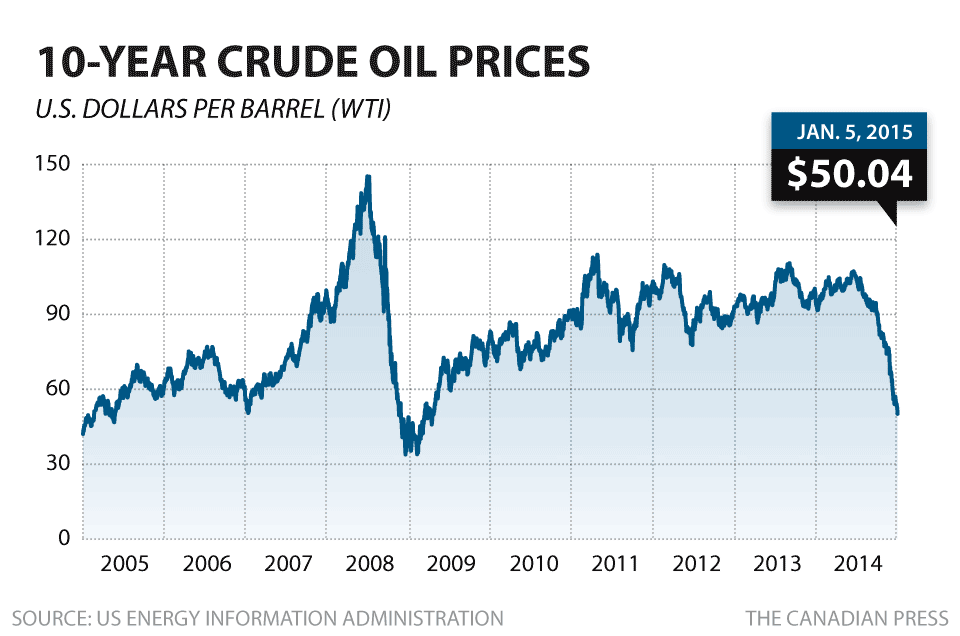

It was admitted that the falling global oil prices, starting from the second quarter of last year (June, 2014), were making it hard for the oil majors to survive.

We have seen a decline in our crude oil price from $140 per barrel in June, 2014 to $55 per barrel in December, 2015. For Nigeria, 95 per cent of our foreign currency comes from oil; so clearly, once you see such depletion, a reduction in price of crude oil, you will expect to see a gradual decline in our external reserves.

Therefore, as our crude oil continues to fall in price at international market, the foreign currency accruable began to slide at an alarming rate and further pressure is exerted on the Naira as a result of the demand for foreign currency by our economy and at that point, the devaluation of the Naira was inevitable.

The Central Bank of Nigeria (CBN), the regulator of the fiscal and monetary policies, at that point, felt that the devaluation of the Naira was expedient to bring a respite to our bloated economy. The oil price given our mono-product economy, investors tend to look at what oil is doing as a barometer to gauge the economy of Nigeria.

Total Nigeria Plc, a marketing and services subsidiary of Total is a pacesetter in the downstream sector of Nigeria Oil & Gas.

It commissioned its first filling station at Herbert Macaulay street, Yaba, Lagos in 1956. It has extensive distribution network of over 500 service stations nationwide and a wide range of top quality energy products and services. The company also enjoys bulk storage facilities at Apapa, Ibafon, Kaduna, Kano and Bukuru depots.

Major Business Activities: involves the finding, extracting, producing and exporting petroleum and gas. It is also engaged with the blending of lubricants and the sales of petroleum products.

Total upstream activities are carried out by 3 subsidiary companies in Nigeria namely Total E&P Nigeria Limited (TEPNG), Total upstream Nigeria Limited (TUPNI) for Oil & Gas, and TOTAL LNG Limited for Gas. The Company has a technical service agreement with Total Outre-Mer (now called Total Africa Middle East) which is renewable every 3 years subject to the approval of The National Office for Technology Acquisition and Promotion (NOTAP).

Financial Highlights: Despite the adverse macro-economic factors prevalent in the year under review, it achieved a growth in turnover and in general terms, it was an impressive performance. In the company’s audited result, its turnover grew by +1.0% from N238.163 billion in the preceding year to N240.618 billion. However, its profit after tax depreciates by -17.00% from N5.334 billion in the preceding year to N4.423 billion. Its Net Assets grew by +5% from N13.240 billion previously to N13.929 billion. Consequently, its board has recommended a mouth-watering dividend of N11.00 per share same as last year (N2.00 per share interim dividend and N9.00 per share final dividend).

The Company’s dividend policy is robust and in total support of Modigliani and Miller’s dividend relevance supposition which states that “the level of dividend payment is a parameter in determining the intrinsic value of a stock and a signal of what to expect in future”.

Apart from the mouth-watering dividend, its fortune on the Stock Exchange as regards capital appreciation is also phenomenal.

The company’s first quarter profile 2015 was still hampered by the same factors that affected its audited result. It will be safe to say that it was a fall-out from the last year’s challenges that impacted negatively on its outcome. The late payment of subsidy (just received) is a typical case. In all, it was a no growth situation against previous year. The 1st quarter result 2015:

Its revenue slide by -1% to N60.042 billion compared from N60.595 billion same period in 2014

Profit before tax decreased by -63% to N625.531 million compared from N1.709 billion previously and

Profit after tax slumped by -79% to N223.217 million compared from N1.069 billion recorded in 2014.

Earnings per Share (EPS) is 66 kobo from 315 kobo, a decrease of -79%

Net Assets leapt by 2% to N14.152 billion from N13.929 billion.

Corporate Governance: The company has a robust board comprising of 10 (ten) members. Board Chairman is Mr. Momar Nguer (Senegalese). The Managing Director is Alexis Vovk. Other members are Mr. Wilfried Konde; Engr. Wole Adeyinka; Engr. Kanu Ukonne; Chief Felix Majekodunmi; Tejiro Ibru; Mr. Denis Toulouse; Engr. Rufai Sirajo and Mr. Mathew Soulas.

Shareholding Structure:

Total Number of shareholding = 339,521,837 shares

Total Raffinage Marketing = 209,559,630 (61.72%)

Other shareholders = 129,962,207 (38.28%)

Market Statistics:

Shares in issue= 339,521,837

52 Weeks High= N182.00

52 Weeks Low= N134.05

52 Weeks Change= 35.77%

Last Price= N159.10

P/E Ratio= 12.21

EPS = 13.02930

Price/Book Value= 3.88

Dividend = N11.00 per share.

Market Sensitivity/ Perception: The broker recommendation is to “HOLD” Total Plc shares. The broker is impressed with the full year result, which revealed that profits were ahead of market expectations. The broker argues that, given the strong share price performance since the turn of the year, the shares are now fairly valued.

The broker feels that the company’s +1.00% increase in revenues to N240.618 billion represents a noticeable shift in growth acceleration on previous year. The broker does acknowledge there were a “couple of areas of disappointment” in its result but believes this masks some solid progress which the company has made.

The broker is of the opinion that the firm as a market leader in its sector is well positioned to continue its progress driven by ongoing sales and margin improvement. The broker believes that management will struggle to deliver anything better than low single-digit organic growth and that earning quality is extremely low.

Industry Perspective:

The Oil and Gas industry is a pillar of the Nigerian economy and a major factor in Nigeria’s world standing. A member of OPEC, Nigeria is responsible for approx.

6% of the organization’s annual oil production. TOTAL has been a partner since 1962 in the development of oil and gas in Nigeria, carrying out both Upstream and Downstream activities.