…as cash-strapped shareholders fail to snap offers

The current recapitalization program embarked on by deposit money banks in the country to meet the mandatory new threshold of N500 billion may face unexpected hurdle, as many shareholders of banks are struggling to take up to their rights in some of the rights issues already concluded.

This, it was learnt, may significantly impact the outcomes of the exercise, as most Nigerians are embattled with survival challenges due to the escalating cost of living in the country.

The apex bank in March 2024 announced new minimum capital requirements for banks, pegging the minimum capital base for commercial banks with international authorisation at N500 billion and national banks at N200 billion. It also instructed non-interest banks with national and regional authorisation to increase their capital to N20 billion and N10 billion respectively.

This, the CBN said, aims to create a more robust banking sector capable of withstanding economic shocks and supporting the government’s ambitious goal of achieving a $1 trillion Gross Domestic Product (GDP) by 2030.

However, the Afrinvest ‘2024 Nigerian Banking Sector Report’ has shown that currently, international banks, which include: Access, First Bank, FCMB, GTCO., First Bank, Fidelity, Zenith, and UBA, have together a capital of about N1.3 trillion and would require, at least, N2.2 trillion to reach the new capitalization requirements.

For the National licenced banks, which include: Ecobank, StanbicIBTC, Citibank, Keystone Bank, Standard Chartered, Sterling, Union Bank, Unity Bank, Polaris, Wema Optimus, and Premium trust bank, their gap according to the report is N1.6 trillion in additional capital to get them to N2.2 trillion. The report also showed a N545 billion capital gap for regional banks, N200 billion for merchant banks and N14 billion for non-interest banks.

Presenting the report in Abuja recently, the Chief Executive, Afrinvest Group, Ike Chioke, noted that the gap underscores the challenge of the anaemic growth that the economy of Nigeria has suffered over the last two decades from 2004 to 2024.

Speaking further, Chioke stressed that all other sectors of the economy must be made to grow alongside the banking sector, if the nation must achieve its $1 trillion economy target.

“When you want to think about growing the Nigerian economy to $1 trillion, it’s not just the banks that will need to grow. Every other aspect of the economy needs to grow alongside it”, Chioke stated.

“So the retail earnings that banks have had for many years will not be counted. So you need to raise capital and put it in as paid-up share capital. That’s a very tall order. But that also brings in all sorts of advantages and strengthens the balance sheet, strengthens their credit rating, and makes them stronger to go.

“But at the same time, when they’re raising money, there are all sorts of other challenges in terms of even the current cash reserve ratios, liquidity ratios are quite high. At the same time, you have a government that’s running its budget on a deficit. That means they’re printing more money to put cash into the system.

“And that same cash, you’re trying to quarantine at the central bank. So there are a lot of mixed signals. In the same economy, where many of us feel challenged by the cost of living crisis, all of us are feeling the pinch of inflation, the pinch of exchange rate devaluation, and yet it’s the same little income that we have that we need to put aside and invest it back in stocks, so there are lots of complicated issues that we need to deal with.”

The governor of CBN, Olayemi Cardoso, noted that the banking sector recapitalization exercise requires all commercial, merchants, and non-interest banks operating in the country to increase their paid-in capital to levels considered suitable for their license categories and authorizations to be achieved in 12-24 months.

Cardoso explained that to meet the requirements, a lot of the banks have begun the issuance of ordinary shares, public offers, right issues, private placements, mergers and acquisitions, adding that those, who are not able to meet the current capital category they are in, are allowed to downgrade.

“Meaning, a national bank can downgrade to a regional bank, and yet be, especially serving the Nigerian people. Now, why do we come out with this? Some of the reasons are for macroeconomic development. We’ve just come out of the COVID pandemic, and a lot of businesses went under, and so it’s macroeconomic development across the globe. We also look at the outcome of the stress test.

“This is to remind us that the Central Bank of Nigeria normally carries what we call a stress test, and it is just to check how the financial institutions will react to shocks at different levels in the economy. And we do that, and we give the results. From the results of management, decisions are taken to ensure that in the event that there are various shock levels in the economy, whether the financial institutions will be able to survive,” he said.

“We are also conscious of the fact that the capital that is going to be imported into the country, especially, from foreign direct investors, and we are assuring them, they are working on the policy for that, that in the place that they are not able to be taken up, they will not suffer any form of devaluation loss and they will be able to go back home with their currency and the value as we deploy them into the country.

“Over the past years, between 2010 and 2015, records have shown that investments in bank shares yielded an average of 17% per annum. So, the recapitalization exercise of the Nigerian banking sector is a pivotal strategy aimed at further strengthening the resilience of the Nigerian banks and promoting sound financial systems in Nigeria. Importantly, it will support the government’s goal to achieve a GDP of $1 trillion by 2030,” he said.

However, analysts at Proshare are of the view that the ongoing efforts by the CBN to increase the capital base of banks may not lead to a higher GDP. The economists, explaining their findings, which contradict comments by officials of the current administration, said the assumption associating big banks with larger economies is unproven.

“Policymakers have associated big banks with larger economies and faster-growing gross domestic products, but the assumption is unproven”, the analysts stated.

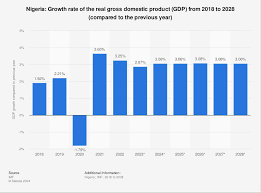

“Nigeria’s GDP in 2005 was N38.78trn and rose to N77.94trn, roughly two times in 2023, suggesting an average annual growth of 3.55% in the last two decades. However, between 2000 and 2005, bank equity sizes grew over 10 times or by 1,150% from N2bn to N25bn.

“In other words, for a decade and a half, banks have used 10 times more equity in their businesses than before 2005, yet the country’s GDP growth has been fairly modest. We must realize that when banks grow bigger, they are not necessarily better. A bigger bank unlocks opportunities for creating larger business value at lower operating costs.”

Weak economy

Recently, PwC, the professional tax and advisory firm, raised fresh concerns about the uncertainties buffeting Nigeria’s economy with negative consequences for investor confidence. Very high inflation and volatility in the forex market have continued defying several measures adopted by the CBN to achieve stability and attract investors.

GDP growth

“Despite the hawkish stance by the CBN to maintain stability, Nigeria’s outlook is still quite uncertain as investors remain cautious of a complex and ambiguous macroeconomic environment,” PwC said in its latest Nigeria Capital market report on August 6.

The FX volatility has introduced significant risks and uncertainties into the business environment. The official exchange rate depreciated by 67.8 per cent from N461.1/$ in May 2023 to N1,433.8/$ in May 2024. It sank to N1,598.9/$ last week.

Business leaders note that uncertainty surrounding the naira’s value has made long-term investment decisions more complex and contributed to a significant level of hesitancy to commit substantial resources in an environment, where currency depreciation could erode returns.

While some quoted companies have had shareholders’ funds eroded by FX losses in the past year, a handful of multinationals have closed shop and fled.

Rising inflation has hit businesses hard, with small companies facing higher costs of raw materials, rent, logistics, and wages that impact profits, making it harder to stay afloat. The situation is worsened by weakened consumer spending power, with average Nigerian now spending about 60 per cent of their income on food.

Inflation increased from 22.41 per cent in May 2023 to 33.95 per cent in May 2024. The drivers include food, utilities, and transportation. Food inflation climbed to 40.6 per cent with utility inflation at 29.6 per cent, and transport inflation at 25.6 per cent according to the NBS.

Taiwo Oyedele, chairman of the presidential committee on fiscal policy and tax reforms in a remark, noted that there was a need to ensure that all sectors of the economy work adequately, stating that available data show that the government has focused its efforts around revenue generation in the wrong places, mostly at the bottom of the ladder

“For you to get a $1 trillion economy, you need the capital market to work, the banking sector is trying to recapitalize, and they also need a capital market themselves. And the capital market needs the economy to work consistently”, he stated.

“So, while we are addressing all the issues around corruption, wasteful spending, inefficiency, we also have to recognize that it’s a fundamental issue that we need to get the economy to work so that revenue can go up.”

Tax burden

Meanwhile, Bank Directors Association of Nigeria (BDAN) has urged the National Assembly to revisit the 70 per cent windfall tax imposed on commercial banks and engage with the lenders on the amendment.

Mustafa Chike-Obi, Chairman, of the Board of Directors, said in a statement that, while the imposition of this windfall tax appears to be a response to the current economic climate, BDAN suggests that a 70 per cent tax rate is excessively burdensome and ill-timed, particularly considering the ongoing bank recapitalisation efforts.

“Such a high levy has the potential to stifle growth and innovation within the banking sector; ultimately affecting the quality of services we provide to our customers and the broader economy,” he said.

But CardinalStone research analysts in their July 22 Model Equity Portfolio (MEP), do not seem to share the sentiment.

“While there are ongoing debates over the legality of a retrospective application of the proposed initiative, our view is that the impact may be relatively minimal since it is to be treated as a one-off tax on FY’23 numbers versus the potential impact if it is applied on a going-forward basis, given the forced realization of FX gains in FY’24 occasioned by CBN’s new Net Open Position (NOP) rule,” the analysts argued.