Economy

Economy plunges under Buhari

- As major economic indicators record negative growth

President Buhari

By UCHE CHRIS

When the economy rebounded in the second quarter of 2017 with a 0.89 percent growth after being in recession for over a year, hope was rekindled that perhaps the country would begin to record some improvements in its economic performance indicators. Exiting recession was good news to government and Nigerians generally, but the hope of any return to the good times was misplaced and soon dashed.

Focus on exiting the recession seemed to have missed the critical challenges facing the economy which caused the recession in the first place. Government as usual had blamed looting by the previous government and crash in oil price for the recession, rather than reviewing the impact of its own economic policies and making adjustments where necessary, as well as addressing underlying weaknesses of the economy.

After three and half years in office, all major economic indicators are southward, a fitting reminder of its abysmal performance in spite of the blame game and corruption fight. Some of the indicators include GDP, inflation, interest rate, debt, unemployment, foreign exchange rate, budget performance, budget deficit, fuel subsidy, and fuel pump price.

After three and half years in office, all major economic indicators are southward, a fitting reminder of its abysmal performance in spite of the blame game and corruption fight. Some of the indicators include GDP, inflation, interest rate, debt, unemployment, foreign exchange rate, budget performance, budget deficit, fuel subsidy, and fuel pump price.

The challenge has been how to get the right policies and the political will to implement them; this is the main undoing of this government. Its focus on corruption and return to state control and disdain for rule of law and fiduciary obligations have created hostile business environment and discouraged investments both foreign and local.

Experts believe that the recession was inevitable as a result of the policy reversals pursued by the government in a period of oil price uncertainty and instability. Recession was only a consequent effect of the continued and long standing mismanagement of the economy that is unproductive, import dependent, oil dependent, corruption ridden and infrastructure deficient.

No economy with these prevailing conditions would ever hope to do well and improve people’s lives. Long before the economy lapsed into recession and at the start of this administration, Dr. Idika Kalu, a former finance minister had described the economy as depressed and required strong reform package to revive it..

As an oil dependent economy its fortunes have always been determined by developments in the oil market. It has happened so many times that it does not require proof. Although government’s vindictive policies accelerated the downward spiral, the economy experienced this down-turn primarily because of the crash in oil price beginning June 2014.

Although, some measure of improvements have been recorded in some sectors of the economy, such as agriculture, which seems to be the focus of government, with the Central Bank of Nigeria, CBN, Anchore Programme, which has seen hundreds of billions of naira pumped into rice production, the economy is still very weak and distressed. It is the upsurge and stability in oil price that is responsible for the half percentile growth as government revenue increases enabling it to meet obligations, and not economic performance that contributed to the exit.

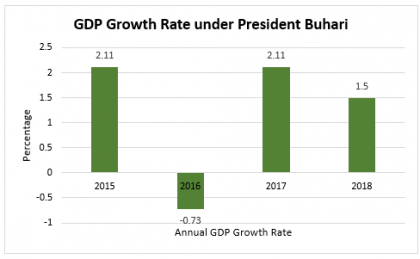

From the available data released by the NBS, GDP performance has never been this appalling in the history of the country, not even during the civil war. Since 1999 Nigeria had grown at above six percent; in 2014 the GDP rate was 7.2 percent. In 2015, it was down to 2.7 percent and then to -2.8 in 2016 and 0.89 in 2017.

Encouraged by this performance, government exuded so much confidence by targeting a rate of 3.5 percent in 2018; this was later revised downward by both IMF and government to 2.7 percent. However, half year report showed a miserable 1.5 percent down from 1.9 in the first quarter.

At about 11.2 percent, inflation is still too high for the economy to improve and the life of people to be relieved. Inflation which was 7.2 in 2014 once rose to 18.2 in 2016 before it dropped. Inflation is one of the major drivers of the hardship ravaging the people. It is a function of the interest rate which has remained high due to massive borrowing.

At about 11.2 percent, inflation is still too high for the economy to improve and the life of people to be relieved. Inflation which was 7.2 in 2014 once rose to 18.2 in 2016 before it dropped. Inflation is one of the major drivers of the hardship ravaging the people. It is a function of the interest rate which has remained high due to massive borrowing.

Furthermore foreign exchange rate of the naira depreciated precipitously from N198 to a dollar in 2015 to the present N360; as an import dependent economy, every imported good went up beyond the reach of average Nigerians.

Where the country is breeding seriously is in subsidy payment. This government promised to end subsidy payment because of the alleged scams that had characterized its operations; it therefore made no provisions in the budget for it. However, with the rise in oil price, the government found itself in dire strait on how to continue to sell fuel at N145 when the landing cost was over N170 per litre.

So the NNPC devised a scheme of what it called under-price recovery and has to source for fund to pay without appropriation; today subsidy has risen from N400 billion in 2015 to N1.3 trillion.

Official interest rate, MPR, has remained at 14 percent for three years but government borrows at 18 percent and practically crowding out the private sector and diverting funds from the real sector as banks just buy government instruments and sit pretty.

Government has tried well to cut down on imports especially of rice and poultry products; however, we still import over 60 percent of our petroleum products consumed locally, which has remained a heavy burden on the value of the naira. Also debt has increased from N11 trillion in 2014 to N23 trillion; government is still expected to borrow $2.3 billion to fund the 2018 budget.

Budget deficit and debt have been the great dereliction of this government. Since coming to power deficit has ballooned from about N400 billion to N2.9 trillion in 2018, compelling government to borrow massively both local and foreign sources to fund the budget.

Budget deficit and debt have been the great dereliction of this government. Since coming to power deficit has ballooned from about N400 billion to N2.9 trillion in 2018, compelling government to borrow massively both local and foreign sources to fund the budget.

Unemployment has also hit the roof-top. When the government took over power, the jobless rate was about six million; at present it is 18 million, three times more. In fact in 2016/17, seven million Nigerians lost their jobs. At 64 percent youth unemployment, there is no magic in the world that can equip government with the enormous challenge of creating jobs for this mass army.

Understandably more Nigerians have joined the extreme poverty category in the past three and half years of this administration. A recent report by the Brookings Institution revealed that 88 million Nigerians now live in extreme poverty of less than one dollar or N360 a day, making Nigeria the world’s poverty capital, ahead of India and China, which are five and six times its population.